Oxirgi ko'tarilishdan keyin oltinda nima kutilmoqda?

.jpeg)

Disclaimer: This content is not intended for EU residents.

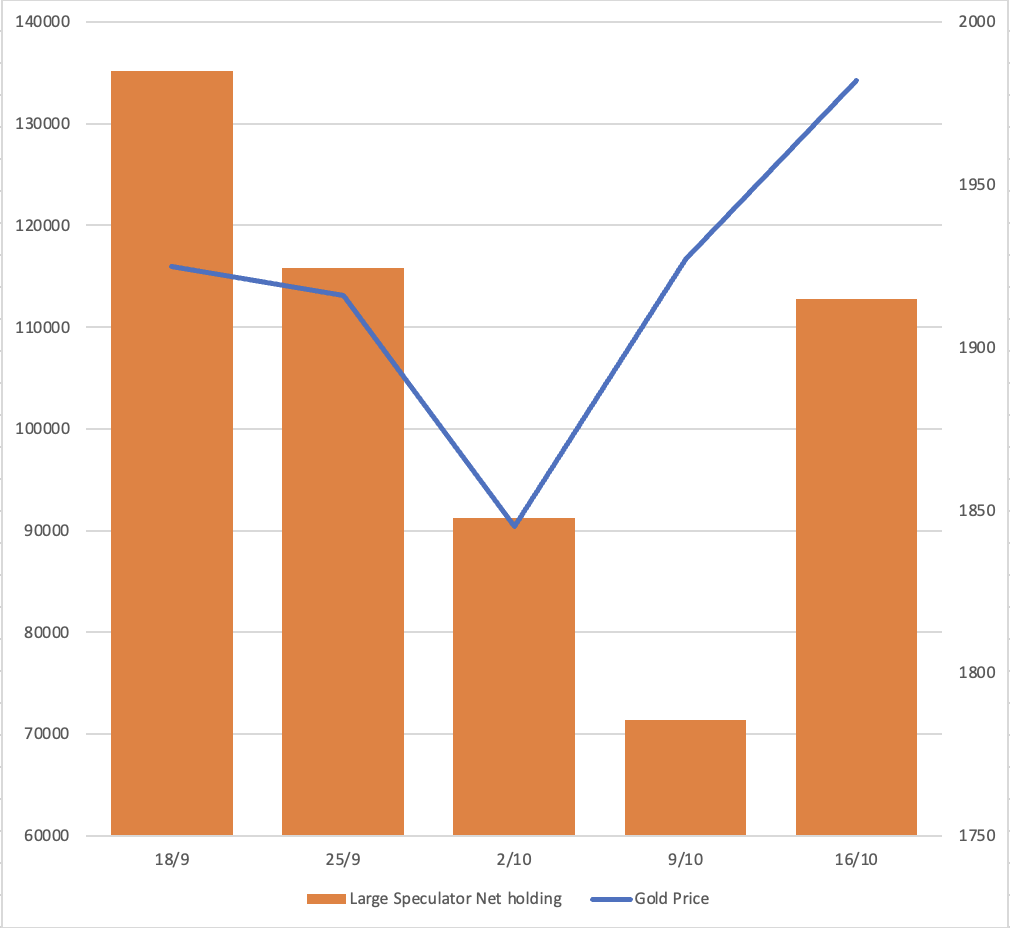

Yaqinda sodir bo'lgan Isroil-Hamas mojarosi oltin ko'tarilishiga sabab bo'ldi, asosan qisqa pozitsiyalarni yopish bilan bog'liq. Endi savol shundaki, bu ko'tarilish davom etishi mumkinmi?

Isroil-Hamas urushi boshlanishidan oldin, COT (Savdogarlarning Murojaatnomasi) hisobotida katta spekulyatorlarning oltin kelajak bozorida qisqa pozitsiyalarda bo'lishi ko'rsatib o'tilgan. Biroq, mojaro davomida faqat ikki hafta o'tgach, bu qisqa pozitsiyalar deyarli yopildi va uzun pozitsiyalarni oshish juda qisqa ko'rsatkichlarni ko'rsatdi. Oltin narxida qancha xavf premiumining hisobga olinganligini baholash qiyin. Davom etayotgan vaziyatning noaniqligi tufayli, qisqa muddatli spekulyatorlar ehtimol ehtiyotkor bo'lib qolishadi va oltinni sotishdan ehtiyot bo'lishadi.

Katta spekulyatorlarning COT hisoboti bo'yicha sof mulk egallashi (Commodity Futures Trading Commission - CFTC)

Oltin xavfsiz aktiv sifatida

Oltin ko'pincha xavfsiz aktiv sifatida hisoblanadi; ammo, 2022 yil 10 martda e'lon qilingan ABN Amro hisobotiga ko'ra, oltinning xavfsiz aktiv maqomi ishonchli emas. Ba'zan oltin xavfsiz investitsiya sifatida harakat qiladi, ba'zan esa xavfga oid aktiv sifatida xususiyatlar ko'rsatadi.

2001 yil 9/11 terror hujumi, 2014 yil Qrim urushi va 2022 yil Rossiya-Ukraína mojarosi kabi tarixiy voqealarga nazar tashlaganimizda, oltin bozorida mos ravishda 6.5%, 11% va 11% ko'tarilishlar muhim namoyish etildi. Hozirda, Isroil-Hamas mojarosi rivojlangan bosqichga etib bormoqda, va Isroil hali erdagi qo'shinlarni joylashtirmagan. Bundan tashqari, agar boshqa davlatlar ushbu mojaroga aralashsa, oltin bozorida allaqachon 7.5% qiymat oshishi sodir bo'lgan. Qo'shimcha oshishlar bo'lsa, oltin yana boshqa ko'tarilishlarni boshdan kechirish ehtimoli mavjud.

Savol tug'iladi: Talab tomonidagi dinamikalar oltin bozorining yo'nalishini shakllantirishda muhim rol o'ynadimi?

Oltin ta'minoti nisbatan barqaror bo'lib qolmoqda, har chorakda 1,100 dan 1,250 tonnagacha doimiy diapazonda olib kelinmoqda. Oltin narxiga ta'sir ko'rsatadigan asosiy omil talab tomonidir, xususan investitsiya talabidir.

Oltin ETFlar ta'minot va talab balansini saqlashda muhim rol o'ynaydi. ETFlardan mablag' chiqishi bo'lsa, bu ko'pincha oltin narxining pasayishiga sabab bo'ladi.

Yuqoridagi diagrammaga qaraganda, oltin ETF kirishlari davomida kuchliroq ko'rsatkichni ko'rsatadi. O'tgan yil davomida Xitoy Markaziy Banki, Turkiya Markaziy Banki va Xitoydagi shaxslar tomonidan oltin sotib olish haqidagi xabarlar olganimizda, 29-sentabr holatiga ko'ra, ETFdan sof chiqimlar hali ham mavjud. Osiyodagi talab qoldiqni boshqa davlatlardan chiqarishga yetarli emas. Oltin juda yaxshi ko'rsatma berdi.

Oltin talabiga ta'sir ko'rsatadigan omillar, xususan investitsiya nuqtai nazaridan nima? Uning maqomi xavfsiz aktiv sifatida, inflyatsiyadan himoya sifatida yoki pul siyosatlarining ta'siri oltin talabini kuchaytiradimi?

- Xavfsiz aktiv

Oldin aytib o'tilganidek, ABN Amro hisobotlari oltinning xavfsiz aktiv sifatida xususiyatlari ishonchli emasligini ko'rsatadi.

- Inflyatsiyadan himoya

Yuqaridagi grafikdan ko'rinib turibdiki, 2000 yildan 2006 yilgacha inflyatsiya past bo'lgan davrda oltin AQSh CPI bilan zaif menga qaramay, -0.055 korelatsiya koeffitsientini ko'rsatdi. Shuningdek, 2007 yildan 2023 yilgacha, oltin inflyatsiya bilan kuchli bog'lanishni ko'rsatmagan bo'lib, 0.36 korelatsiya koeffitsientiga ega.

Masalan, 2020 yilda 2,075 AQSh dollaridagi eng yuqori oltin narxida, 2023 yilda 2% inflyatsiya darajasini taqqoslaydigan bo'lsak, eng yuqori oltin narxi 2,075 AQSh dollarida qoldi, inflyatsiya esa 7% dan oshdi. Agar oltin inflyatsiyaga qarshi samarali himoya bo'lsa edi, biz uning qiymati 2020 yildan oshishini kutgan bo'lardik.

- Pul siyosati

Yuqoridagi grafik oltin va AQSh 3 oylik daromad o'rtasidagi aloqani ko'rsatadi, oltin ni pasayganida o'zini ko'rsatib kelmoqda, 2006 yildan beri ayniqsa.

Savol tug'iladi: Aylanma nuqtasi kelishimiz mumkinmi? Fed stavkalarni ko'tarishda davom etadimi? Agar bozor hissi Fed tomonidan stavkalarni kamaytirish ehtimolini hisobga olgan bo'lsa, bu oltin ko'tarilishining boshlanishini bildirishi mumkin.

Atlanta Fed modeliga ko'ra, uch oylik daromad pasayishni boshlaydi, eng erta prognoz yanvar 2024 yilda, eng kechida esa iyun 2024 yilda bo'ladi.

Oltin va JPY hamda oltin va GBP o'rtasidagi taqqoslash harakat qilayotgan eng yuqori darajalarga yetdi, lekin bu oltinning AQSh dollariga nisbatan yangi rekord darajaga yetishini kafolatlamaydi. Biroq, bu oltin boshqa valyutalarga nisbatan kuchayishni davom ettirishiga ishora qiladi.

Ba'zi hollarda, USD va oltin bir vaqtda ko'tarilgan, bu XAU/USD va USD/EUR grafikida ko'rsatilgan. Qorong'i joylardan bu USD va oltin bir vaqtning o'zida harakatlanib turar.

Texnik tahlil

Diagramma shakli: Uzoq muddatli oltin grafikida, chashka va tutqich shakli hosil bo'lmoqda, chashkaning chap tomoni 2011 yilda hosil bo'lgan. Hozirda oltin tutqichni hosil qilish jarayonida bo'layotgandek ko'rinadi. Agar oltin 2,080 dan yuqori darajada bosib o'tishga muvaffaq bo'lsa, biz yanada ko'tarilishimizni kutishimiz mumkin. Muhim jihati, yordam taxminan 1,800 atrofida kelishi kutilmoqda.

Rad etish:

Savdo xavflidir.

O`tgan natijalar kelajakdagi natijalarning kafolati emas. Har qanday savdo qarorini qabul qilishdan oldin o`zingizning tadqiqotingizni o`tkazish tavsiya etiladi.

Ushbu blog maqolasida keltirilgan ma`lumotlar faqat ta`lim maqsadlarda berilgan va moliyaviy yoki investitsiya maslahati sifatida qaralmagan.

.jpeg)