Is Amazon’s massive AI spend a warning or a buying opportunity?

Amazon’s $200 billion AI spending plan looks dramatic because it arrived at exactly the wrong moment. Markets were already fragile, tech sentiment was wobbling, and US stock futures were pointing lower as investors digested another bruising session on Wall Street.

By the time Amazon reported, the S&P 500 and Nasdaq had slipped into negative territory for 2026, and patience was already thin.

So when Amazon shares plunged more than 10% after the bell - following a marginal earnings miss and a staggering capital expenditure forecast - the market’s verdict came quickly. This was not read as a sign of strategic strength, but as another stress test for investors already bracing for wreckage. The key question now is whether that reaction reflects genuine risk - or a short-term panic that may be missing the bigger picture.

What’s driving Amazon’s AI spending surge?

Amazon’s plan to invest around $200 billion in 2026 is not incremental spending. It is a deliberate acceleration across data centres, custom chips, robotics, logistics automation, and low-Earth-orbit satellite infrastructure. That figure dwarfs the roughly $125 billion spent in 2025 and comfortably exceeds analysts’ expectations, forcing markets to recalibrate assumptions in real time.

Crucially, Amazon insists this is demand-led. AWS revenue rose 24% year on year to $35.6 billion - its fastest growth in 13 quarters - as customers ramped up both core cloud workloads and AI adoption. CEO Andy Jassy was blunt on the earnings call: capacity is being monetised as fast as it can be installed. In other words, Amazon is not building empty data centres. It is racing to keep up.

Still, context matters. This spending landed in a market already leaning risk-off. Amazon’s slide rippled across tech, dragging sentiment lower as investors reassessed AI exposure more broadly. The reaction spilled into other assets too: bitcoin slid to levels not seen since 2024, silver resumed its decline after a retail-fuelled surge, and Strategy (formerly MicroStrategy) revealed a quarterly loss driven by crypto weakness. This was not a calm market parsing nuance - it was one looking for reasons to de-risk.

Why did the market react so sharply?

On the surface, Amazon’s earnings were not alarming. Revenue beat expectations at $213.4 billion. AWS and advertising both topped forecasts. The earnings-per-share miss - $1.95 versus $1.97 expected - was trivial by historical standards.

But this earnings season is being judged differently. Investors are no longer rewarding scale alone. They want visibility on cash returns, especially as AI infrastructure bills balloon. Amazon’s free cash flow over the past 12 months fell to just $11.2 billion, despite operating cash flow rising 20% to $139.5 billion. The culprit is not weak operations, but capital intensity. AI spending is already compressing the numbers investors underwrite.

Guidance compounded the unease. First-quarter operating income is expected to come in below consensus, with management flagging roughly $1 billion in additional year-on-year costs tied to infrastructure and satellite expansion. In a market already unsettled by softening labour data - job openings at their lowest since 2020 and layoffs accelerating - Amazon’s timing could hardly have been worse.

Broader market fallout adds to the pressure

Amazon’s sell-off did not happen in isolation. While Reddit and Roblox surged on earnings beats and upbeat guidance, those moves felt like exceptions rather than the rule. The broader tone remained defensive, with investors increasingly selective about where they were willing to take risks.

Macro uncertainty is adding another layer. The nonfarm payrolls report, delayed to next week after the resolution of the US government shutdown, now looms larger than usual. Recent data has already hinted at cracks in the labour market, and any downside surprise could reinforce fears that corporate spending - including on AI - is running ahead of economic reality.

In that environment, Amazon’s decision to double down on long-term infrastructure reads less like confidence and more like defiance. The market is not questioning whether Amazon can spend. It is questioning whether this is the right cycle to ask investors to wait.

Is this a familiar Amazon playbook or something new?

Amazon has been here before. Its history is built on spending ahead of demand, absorbing scepticism, and emerging with structural advantages that competitors struggle to replicate. Prime, fulfilment automation, and AWS itself all followed that script.

AI, however, changes the scale. This time, Amazon is not alone. Microsoft and Alphabet are spending heavily, too, which compresses early-mover advantage and stretches payback timelines. The competitive moat forms more slowly when everyone is building simultaneously.

That said, Amazon is not merely a buyer in the AI ecosystem. Through Annapurna Labs, it has developed a substantial in-house chip business. Custom processors such as Trainium and Graviton now generate a combined annual revenue run rate above $10 billion, helping offset dependency on third-party suppliers and laying the groundwork for future margin expansion. That internal capability may prove critical once the spending phase peaks.

Expert outlook: Warning sign or opportunity?

This does not look like a balance-sheet warning. Amazon generated $77.7 billion in net income in 2025 and retains ample financial flexibility. The real risk is narrative drift - allowing markets to frame AI spending as unchecked ambition rather than disciplined expansion.

For short-term investors, discomfort is justified. Cash flow is under pressure, sentiment is fragile, and the macro backdrop is deteriorating. Volatility is likely to persist until the market clarifies when AI spending will moderate.

For long-term investors, the sell-off raises a different question. If AWS demand remains strong and infrastructure utilisation stays high, today’s spending could underpin years of pricing power and operating leverage. Amazon is asking the market to fund capacity now in exchange for dominance later. History suggests that trade has often worked - but it rarely feels comfortable at the time.

Key takeaway

Amazon’s massive AI spend is not a signal that the business is faltering. It is a signal that the market’s tolerance for long-dated payoffs has sharply diminished. The company is choosing to invest through a risk-off cycle, not retreat from it. Whether this proves to be a warning or a buying opportunity will hinge on execution, cash flow recovery, and how quickly AI demand translates into visible returns. The next few quarters will tell whether this sell-off reflects discipline or short-sighted fear.

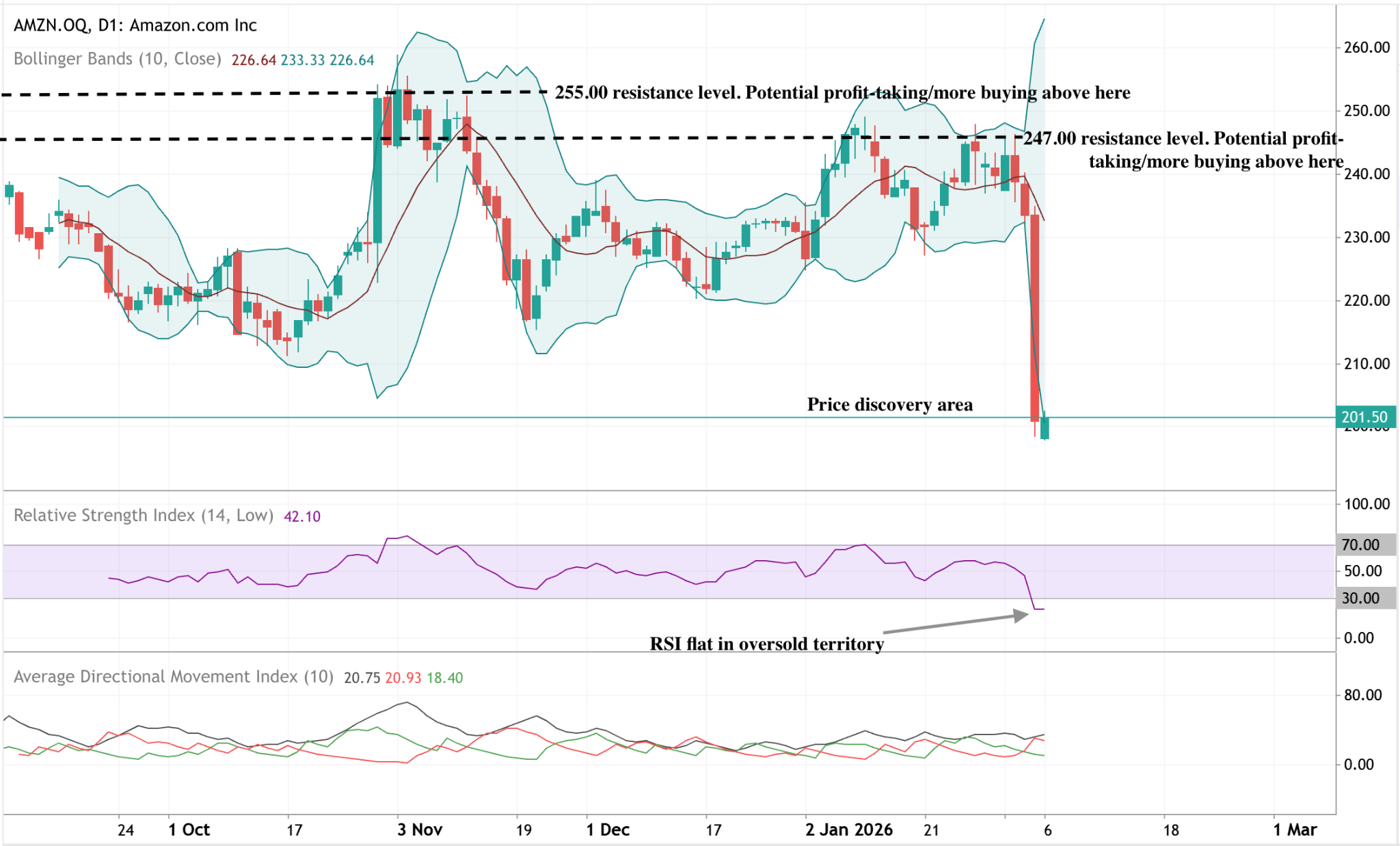

Amazon technical outlook

Amazon has experienced a sharp downside move, with the price breaking lower from its recent range and falling toward the lower end of the charted structure. Bollinger Bands have expanded significantly following the decline, indicating a sudden increase in volatility after a period of more contained price action.

Momentum indicators reflect the intensity of the move: the RSI has dropped into oversold territory and is currently flat at low levels, signalling persistent downside momentum rather than an immediate stabilisation. Trend strength readings show limited directional dominance, with ADX remaining relatively subdued despite the sharp price adjustment.

Structurally, price has moved well below prior resistance areas around $247 and $255, placing recent action in a new price range relative to the earlier range.

The performance figures quoted are not a guarantee of future performance.

The future performance figures quoted are only estimates and may not be a reliable indicator of future performance.