Oil outlook: Why geopolitics isn’t enough to lift crude

.png)

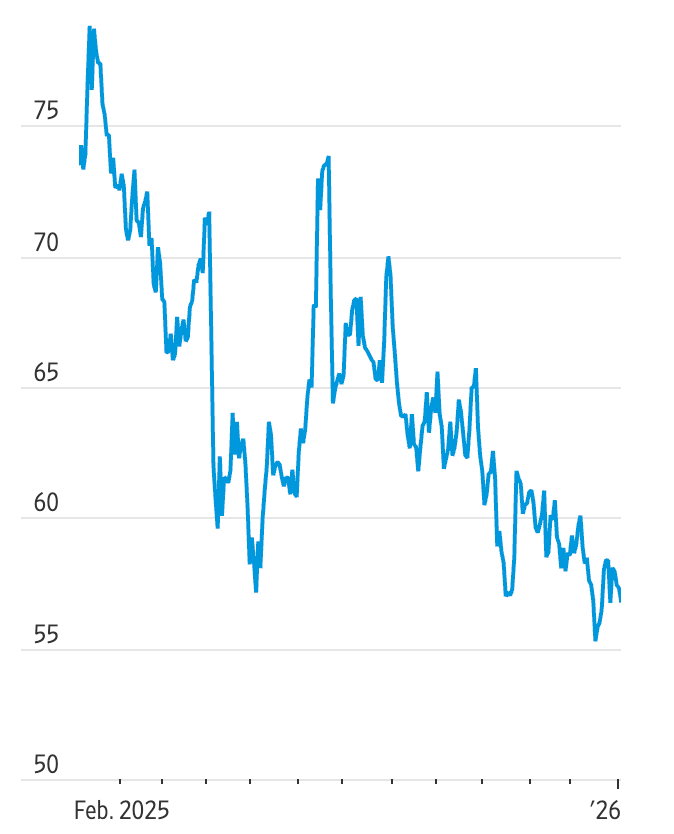

Geopolitical shocks once sent oil prices sharply higher, but analysts say that playbook no longer works on its own. Despite the dramatic removal of Venezuela’s President Nicolás Maduro and President Donald Trump’s pledge to send US oil majors back into the country, crude prices barely reacted. US benchmark oil hovered near $57 a barrel, while Brent traded just above $60, levels close to five-year lows.

According to analysts, the explanation lies in market structure rather than politics. Global supply remains abundant, demand growth is subdued, and spare capacity elsewhere can absorb disruptions. Until that balance changes, geopolitical events may generate headlines, but they struggle to generate sustained upside for crude.

What’s driving oil prices?

The dominant force shaping the outlook for oil is oversupply. The global market is already dealing with excess barrels as OPEC+ holds output steady and non-OPEC producers, led by the United States, continue pumping at or near record levels. US crude prices fell by around 20% last year, underscoring the resilience of supply in the face of softer consumption trends.

Venezuela’s political shift adds uncertainty, but not immediate scarcity. The country currently produces roughly 800,000 to 1.1 million barrels per day, down from more than 3.5 million barrels per day at its peak in the late 1990s. Even optimistic scenarios assume a slow recovery, requiring years of investment and stable governance before meaningful volumes return to global markets.

Why it matters

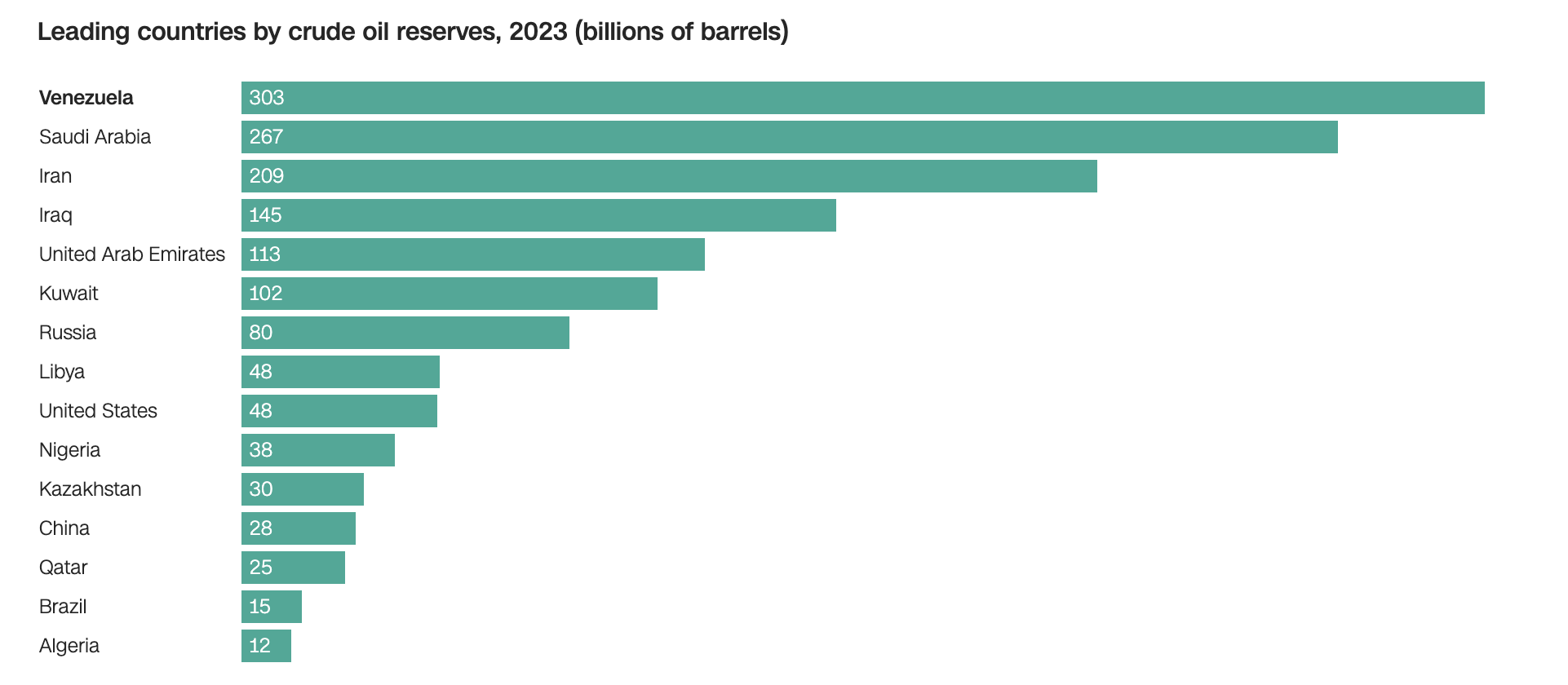

For traders and policymakers alike, timing is critical. Oil markets price what can be delivered now, not what might be produced in five years. While Venezuela holds the world’s largest proven crude reserves at 303 billion barrels, those reserves remain constrained by deteriorated infrastructure, sanctions, and political risk.

Goldman Sachs’ head of oil research, Daan Struyven, has described the impact of Maduro’s removal as ambiguous in the near term. Sanctions relief could eventually lead to increased output, but short-term disruptions remain possible, and any recovery is likely to be gradual. In the meantime, surplus conditions continue to dominate the price formation process.

Impact on the Oil market

The practical implication is a ceiling on prices rather than a floor. Analysts estimate that even full sanctions relief could bring back only several hundred thousand barrels per day over the first year, assuming an orderly transition of power. That increase would be easily offset by marginal supply growth elsewhere.

This dynamic explains why Brent briefly dipped below $61 before stabilising and why volatility has remained contained. As Capital Economics noted, any Venezuelan disruption can be absorbed by spare capacity, particularly since OPEC+ is unlikely to tighten supply aggressively while demand growth remains uncertain.

Expert outlook

Looking ahead, analysts largely expect oil to remain range-bound with downside risks. Capital Economics forecasts that crude prices will drift towards $50 a barrel over the next year as global supply growth continues to outpace demand. A successful Venezuelan recovery would reinforce that trajectory rather than reverse it.

The key uncertainty is execution. Industry executives estimate it would cost around $10 billion a year to rehabilitate Venezuela’s oil sector, and only a stable political environment would unlock that capital. Until investors see credible reforms and lasting sanctions relief, Venezuelan oil remains a long-term story in a market focused on near-term balances.

Key takeaway

Geopolitical drama no longer guarantees higher oil prices. With global supply abundant and Venezuelan output years away from a meaningful recovery, fundamentals continue to cap crude’s upside. Until demand strengthens or producers cut supply more aggressively, analysts expect oil to remain under pressure. Traders should watch sanctions policy, OPEC discipline, and US production data for the next decisive signal.

Oil technical outlook

US oil remains under near-term pressure as price struggles to regain traction above the 57.47–58.40 resistance zone, keeping the broader structure tilted to the downside. Recent attempts to stabilise have been met with renewed selling, and price is now hovering just above the 56.40 area, with the 55.37 support acting as a key downside pivot.

Momentum indicators reinforce this cautious outlook: the RSI has dipped below the midline, signalling weakening bullish momentum, while price continues to trade below the key resistance cluster. Bollinger Bands suggest volatility remains elevated, but without clear directional conviction.

A sustained break below 55.37 could open the door to deeper liquidation-driven selling, while any recovery would need a decisive move back above 58.40 to shift the short-term bias.

The performance figures quoted are not a guarantee of future performance.