Retail trader inflows raise the stakes for Nvidia earnings

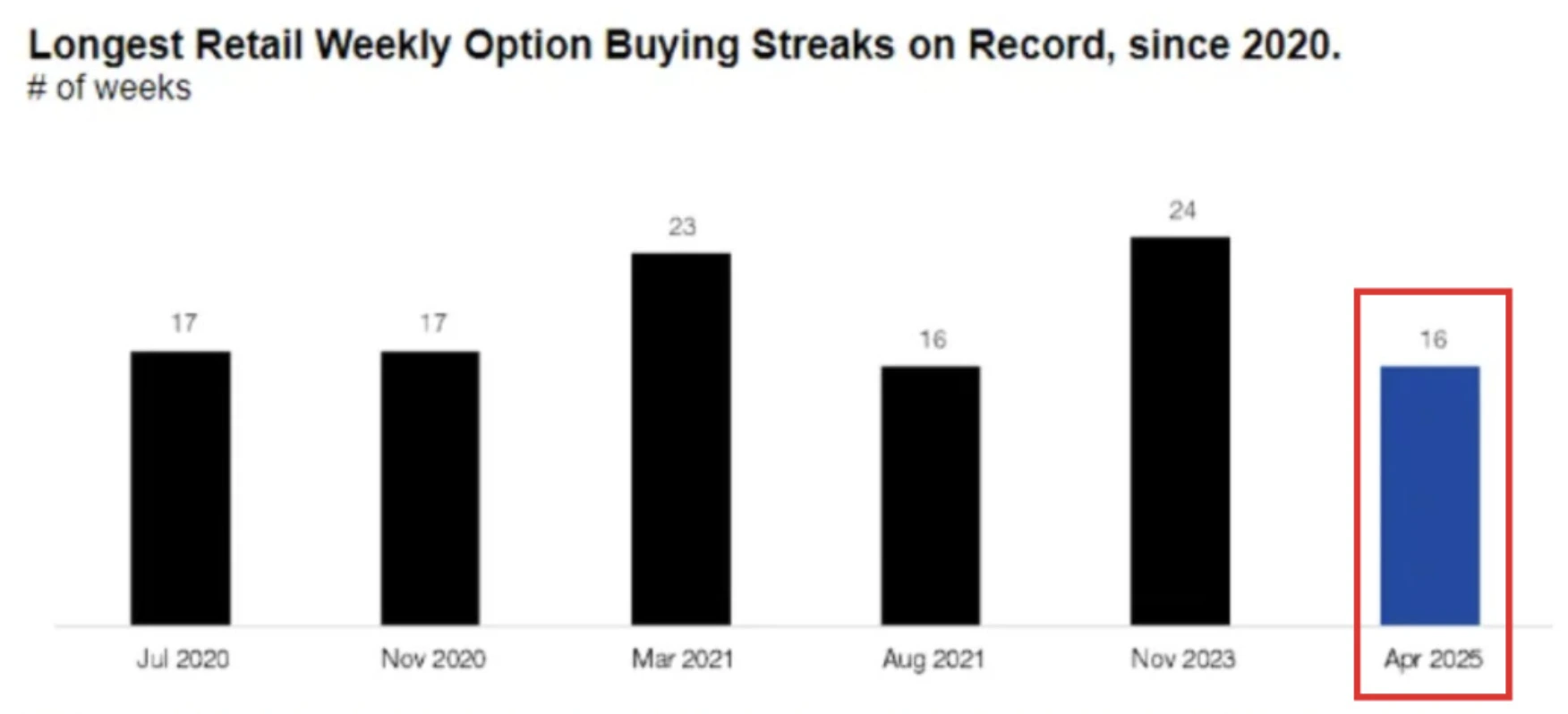

Retail traders have fuelled a historic 16-week streak of net equity buying - the longest since 2020 - with Nvidia as one of their top targets ahead of its 27 August fiscal Q2 2026 earnings release. Consensus estimates stand at $45.9 billion in revenue and $1.00 in adjusted EPS, but Nvidia’s stock has already climbed 83% since April. That rally, combined with heavy retail inflows, sets a high bar. The key test is whether strong results and guidance can keep retail momentum intact, or if disappointment triggers a meme-style pullback.

Key takeaways

- Retail investors have been net buyers of Nvidia for weeks, making it July’s most purchased stock on Charles Schwab platforms.

- Nvidia’s Q2 revenue consensus is $45.9B, slightly above its $45B guidance that excluded an $8B China headwind from H20 restrictions.

- A newly granted U.S. licence for H20 shipments to China could allow Nvidia to recover part of that lost revenue.

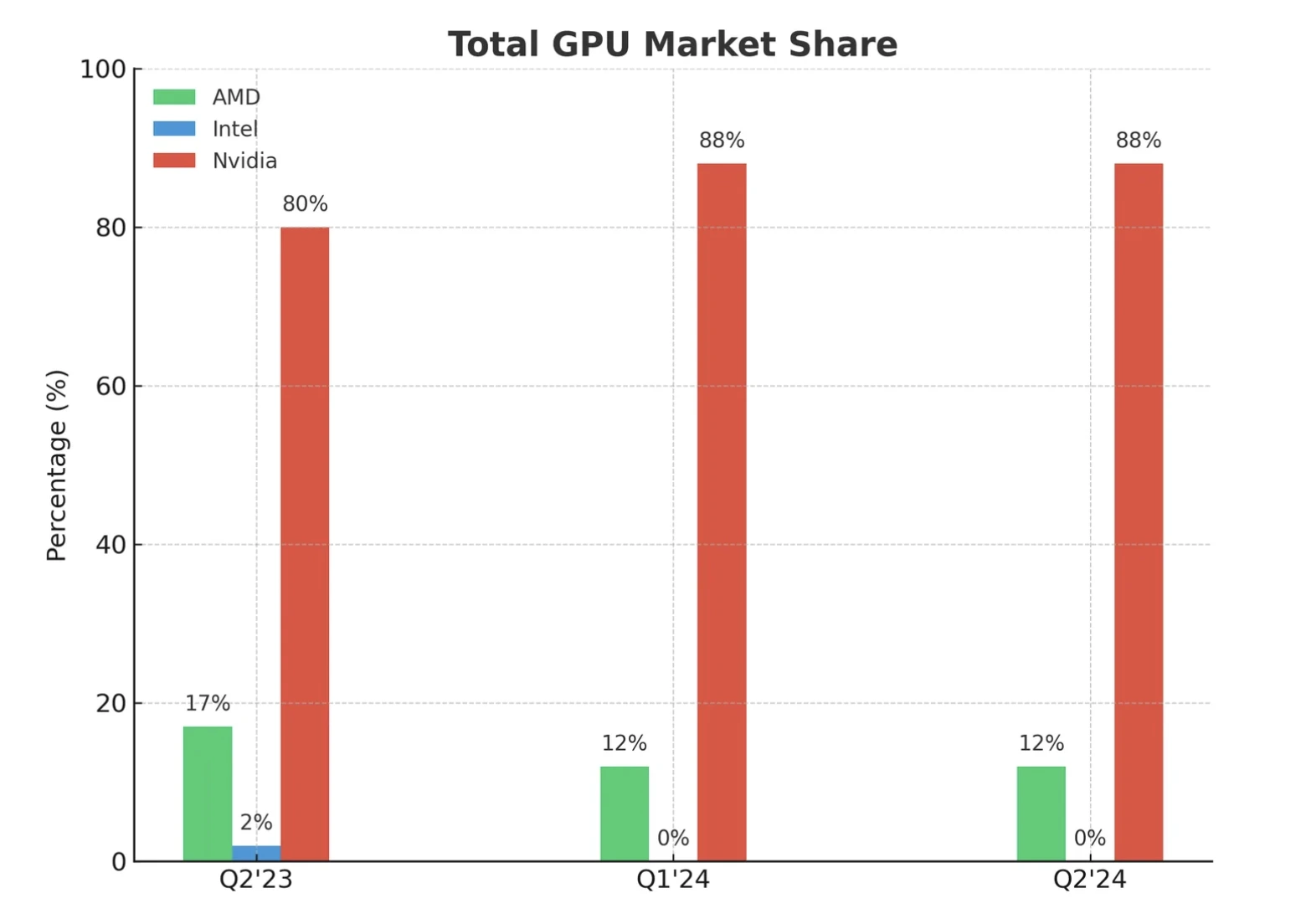

- Hyperscalers are projected to spend $364B on capex in 2025, up sharply from $325B, underpinning Nvidia’s 80% AI chip market share.

- Retail inflows contrast with institutional caution, as speculators hold their largest short positions in $SPY this year.

- Nvidia trades at 58x earnings, more than double the S&P 500, leaving little room for error if guidance disappoints.

Retail trader flows set up a high-stakes earnings event

According to Citadel Securities, retail traders have been net buyers of equity options for 16 straight weeks, the sixth-longest streak since 2020. Nvidia and Tesla are central to this activity, with UnitedHealth also ranking high on retail flows.

In July, Nvidia was the single most-bought stock by retail clients at Schwab.

This activity mirrors the meme-stock era of 2020 - 2021, but with two key differences:

- Retail demand is concentrated in mega-cap tech rather than smaller speculative names.

- Investors are using commission-free platforms and API-driven data access to trade more strategically.

The result is that Nvidia enters its earnings call not just as a corporate bellwether, but as a test case for whether retail flows can sustain tech valuations at record highs.

Nvidia earnings preview and the AI chip market share

When Nvidia released Q1 results, it guided for $45B in Q2 revenue, while warning of an $8B hit tied to U.S. restrictions on its China-specific H20 chip. The restrictions led to a $2.5B revenue loss and a $4.5B charge in Q1.

Since then, developments have shifted:

- Licence reinstatement: In July, the U.S. Commerce Department granted Nvidia approval to ship H20 chips to China, on the condition that 15% of sales revenue be remitted to the government.

- Timing impact: Applications began on 15 July, two weeks before the quarter closed. Some H20 revenue may therefore appear in Q2, with more upside potential in Q3.

- Demand backdrop: Despite ongoing U.S. - China tensions, AI chip demand in China remains acute due to supply shortages, suggesting strong uptake for the H20.

Beyond China, hyperscaler investment remains the dominant growth driver. Amazon, Microsoft, Meta, and Alphabet are projected to lift 2025 capex to $364B, a 64% YoY jump and 5 percentage points faster than 2024. With Nvidia steadily controlling ~80% of the AI GPU market, this spending spree is effectively a direct revenue pipeline.

Retail vs institutional positioning

The contrast between retail enthusiasm and institutional hedging is stark. Retail traders continue to rotate into Nvidia, but CFTC data show speculators are heavily short $SPY, reflecting broader caution on U.S. equities. Morgan Stanley analysts note that while demand indicators are “remarkable, insatiable, massive”, supply chain factors remain the near-term bottleneck.

This divergence raises the stakes: if Nvidia beats, retail momentum could amplify gains. But if results or guidance disappoint, heavy retail positioning could flip into a sharp unwind. Historical parallels with GameStop and AMC suggest that retail-fuelled rallies often end abruptly once momentum fades.

Valuation and risk of a pullback

Nvidia’s valuation underscores the tightrope. At 58x forward earnings, it trades at more than twice the S&P 500’s 25x. Bulls argue this premium is justified by expected EPS growth of +47% YoY in Q2, more than five times the index average.

Still, the setup is binary:

- Upside case: Q2 revenue tops guidance as H20 exports resume, capex guidance rises, and Blackwell architecture transition runs smoothly. Stock could push past $200 resistance.

- Downside case: Conservative commentary on China, or weaker-than-expected data centre trends, could spark profit-taking. A drop toward $175 support would align with seasonal retail slowdowns seen in late summer.

Market impact and price scenarios

- Bullish outcome: Earnings surprise to the upside, retail inflows sustain momentum, and Nvidia extends its 83% rally since April.

- Bearish outcome: Guidance stays conservative, institutional shorts gain traction, and retail enthusiasm fades - sharp correction.

- Volatility outcome: Large positioning on both sides drives oversized post-earnings moves, regardless of direction.

Nvidia technical analysis

At the time of writing, the stock price is seeing a significant dip after bouncing off a resistance level - hinting at a potential further dip. However, volume bars show dominant bullish pressure with sellers not pushing with enough conviction. Should a further drawdown materialise, prices could find support at the $169.00 and $142.00 levels. If we see an uptick, on the other hand, prices could face resistance near $183.75.

Investment implications

For traders, Nvidia’s 27 August earnings are not just about one company - they are a test of whether retail flows can keep powering U.S. tech higher. Short-term strategies should anticipate volatility around $175–$200 technical levels.

Medium-term positioning hinges on whether Nvidia can turn reinstated China exports and accelerating hyperscaler spending into earnings momentum that validates its premium multiple. Retail traders have set the stage. Nvidia’s results will decide whether the rally extends or gives way to a correction.

What will happen to Nvidia's prices after the earnings release? Speculate on its next movements today with a Deriv MT5 account.

Frequently asked questions

Why are retail traders so focused on Nvidia?

Because it offers the cleanest exposure to AI infrastructure, with unmatched dominance in GPUs for data centres.

What could make earnings stronger than expected?

China H20 licence sales, higher hyperscaler spending, and accelerating sovereign AI infrastructure demand.

What are the biggest risks?

High valuation, conservative guidance, and volatility if retail inflows reverse.

How does Tesla relate to this trend?

Tesla is the other main beneficiary of retail flows, alongside Nvidia, making both central to the broader retail-driven tech rally.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.