Prognoza S&P 500: Czy rynek poradzi sobie z ograniczoną płynnością?

Krótka odpowiedź brzmi: tak – ale nie bez napięć. S&P 500 wciąż utrzymuje się blisko rekordowych poziomów, jednak pod powierzchnią płynność rynkowa kurczy się w sposób, który historycznie utrudnia utrzymanie wzrostów na rynku akcji.

W samą środę indeks referencyjny spadł zaledwie o 0,5%, podczas gdy równoważony S&P 500 wzrósł prawie o 0,9%, co spowodowało, że rozbieżność na rynku zbliżyła się do górnej granicy swojego historycznego zakresu.

To istotne, ponieważ to płynność, a nie zyski, coraz bardziej nadaje ton rynkowi. Wraz z końcem sezonu wyników, rentowności długoterminowych obligacji oscylującymi w pobliżu oporu oraz przygotowaniami US Treasury do odprowadzenia gotówki z systemu, zdolność rynku do absorpcji zaostrzonych warunków finansowych zdefiniuje kolejny etap trajektorii S&P 500.

Co napędza prognozy dla S&P 500?

Ostatnie ruchy cenowe pokazują rynek rozrywany w dwóch kierunkach jednocześnie. Akcje technologicznych gigantów ciążyły głównemu indeksowi S&P 500, podczas gdy mniejsze spółki i sektory defensywne po cichu zyskiwały.

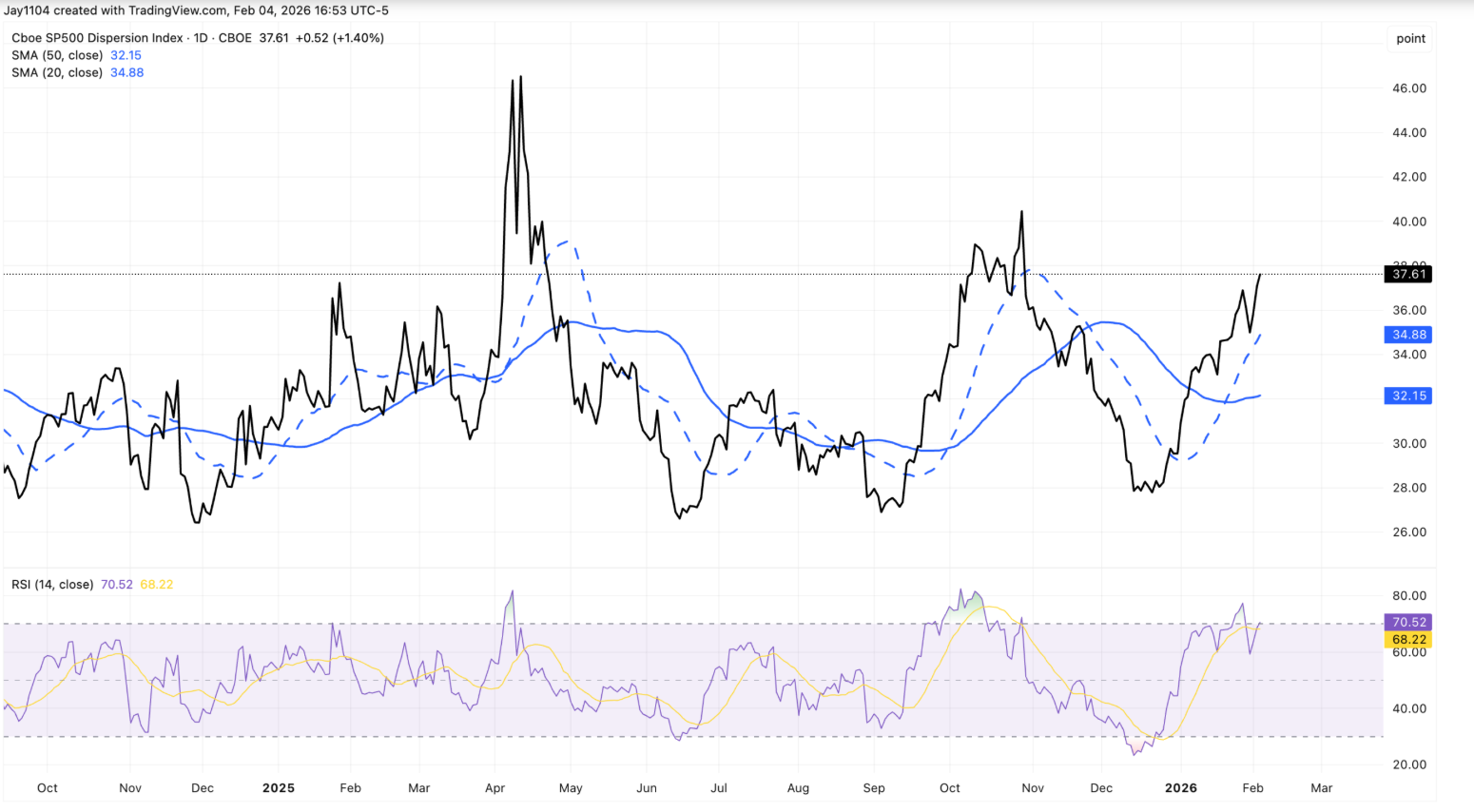

Efektem był gwałtowny wzrost rozbieżności, a indeks dyspersji wzrósł do około 37,6 – poziomu częściej kojarzonego ze szczytową zmiennością zysków niż z końcem sezonu raportowania.

Jedno z wyjaśnień leży w pozycjonowaniu, a nie w przekonaniu. Wskaźnik zmienności implikowanej rośnie bardziej agresywnie niż w poprzednich kwartałach, zachęcając inwestorów do wybierania stabilnych profili zysków, takich jak dobra konsumpcyjne podstawowe. Utrzymująca się siła Walmartu, mimo że spółka nie raportuje wyników aż do połowy lutego, odzwierciedla to zachowanie. Zamiast czystej rotacji sektorowej, ruch ten przypomina te same transakcje dyspersyjne, które dominowały na rynkach przed publikacją wyników największych spółek technologicznych.

Rynki obligacji wzmacniają to niepewne tło. Rentowność 30-letnich obligacji skarbowych USA ponownie zbliżyła się do poziomu 4,9%, po raz kolejny testując górną granicę, która od tygodni ogranicza wzrosty rentowności.

W normalnych warunkach duża podaż, utrzymujące się deficyty i odporność wzrostu gospodarczego powinny zdecydowanie podnieść rentowności. Tymczasem stopy wydają się zamrożone, co sugeruje, że to ograniczenia płynności – a nie optymizm – kotwiczą rynki w miejscu.

Dlaczego to ważne

Dla inwestorów ta rozbieżność jest sygnałem ostrzegawczym. Gdy powierzchowna stabilność S&P 500 maskuje wewnętrzne napięcia, rynki stają się bardziej podatne na nagłe zmiany wycen. Siła indeksu równoważonego przy jednoczesnej słabości indeksu ważonego kapitalizacją sugeruje selektywną redukcję ryzyka, a nie szerokie zaufanie do przyszłego wzrostu.

Dynamika płynności potęguje to ryzyko. US Treasury sygnalizuje, że Treasury General Account może przekroczyć 1 bilion dolarów w okolicach sezonu podatkowego, co oznacza wycofanie z rynku około 150 miliardów dolarów dodatkowej gotówki.

Chociaż zwiększona emisja bonów skarbowych może złagodzić ten efekt, analitycy są zgodni, że nie zrekompensuje ona w pełni odpływu środków. Jak zauważyła Sonali Basak z iCapital, rynki nie wyceniają szoku, ale „płynność nie zapewnia już takiego wsparcia jak w zeszłym roku”.

Wpływ na rynki i inwestorów

Najbardziej bezpośrednim efektem była agresywna rotacja sektorowa. Technologia, zwłaszcza oprogramowanie, najbardziej ucierpiała podczas środowej wyprzedaży, gdy obawy o zakłócenia związane ze sztuczną inteligencją i wysokie wyceny skłoniły inwestorów do ograniczenia ekspozycji. Nasdaq Composite spadł o 1,5%, podczas gdy Dow Jones Industrial Average zyskał 0,5%, co podkreśla, jak bardzo przywództwo na rynku stało się nierówne.

Jednocześnie długoterminowa narracja AI pozostaje nienaruszona. Wyniki Alphabet podkreśliły plany zwiększenia nakładów inwestycyjnych nawet do 185 miliardów dolarów do 2026 roku, co wsparło Nvidia i Broadcom, mimo że akcje Alphabet nieco spadły. Reakcja rynku sugeruje, że inwestorzy raczej ponownie oceniają krótkoterminowe wyceny niż całkowicie porzucają temat AI.

Dla inwestorów długoterminowych ryzyko tkwi w samozadowoleniu. Jeśli płynność będzie się dalej kurczyć, a stopy pozostaną blisko oporu, zmienność może powrócić gwałtownie, gdy korelacje wzrosną, a transakcje dyspersyjne zostaną zamknięte.

Prognozy ekspertów

Patrząc w przyszłość, wielu strategów oczekuje, że rozbieżności rynkowe zanikną wraz z końcem sezonu wyników i zamykaniem pozycji taktycznych. Historycznie korelacje rosną, gdy niepewność co do zysków mija, co przywraca spójność wyników sektorów. Sam ten proces może zwiększyć zmienność, nawet bez szoku makroekonomicznego.

Największą niewiadomą pozostaje płynność. Cotygodniowe dane o nowych bezrobotnych, wyniki Amazon oraz aktualizacje dotyczące finansowania Treasury będą uważnie obserwowane. Utrzymujące się wybicie powyżej 5% w przypadku 30-letnich obligacji prawdopodobnie wywarłoby presję na wyceny akcji, podczas gdy dalsza stagnacja stóp może sygnalizować głębsze napięcia na rynku finansowania. Na ten moment S&P 500 jest w stanie zaabsorbować bardziej ograniczoną płynność – ale tylko tak długo, jak utrzyma się zaufanie.

Najważniejsze wnioski

S&P 500 jest w stanie przetrwać obecnie bardziej ograniczoną płynność, ale margines bezpieczeństwa się kurczy. Rozbieżności w indeksie, uporczywe rentowności obligacji i nadchodzące odpływy gotówki sugerują, że stabilność może być złudna. W miarę jak zyski schodzą na dalszy plan, płynność stanie się kluczowa. Kolejny decydujący ruch najprawdopodobniej nie będzie wynikał z zysków, lecz z warunków finansowania.