Trump tariff impact on currencies: Will his strategy backfire?

According to analysts, the Japanese Yen has hit a two-week low against the US dollar, with USD/JPY climbing above 149.50 during Tuesday's Asian session. This marks the third straight day of losses for the Yen, as global risk appetite improves on the back of China's economic stimulus efforts and hopes for progress in Ukraine peace talks.

Trump’s trade policies and global currency shifts

Analysts also note that Donald Trump's second presidency is having a dramatic impact on global currencies-though not in the way investors initially expected. The U.S. dollar has weakened this year against most major developed market currencies, with the exception of the Canadian dollar, as concerns grow that tariff uncertainty is harming the U.S. economy.

Tariffs are often expected to strengthen the dollar, but when imposed on close trading partners, they can weaken confidence in the U.S. economy. As recession risks in the U.S. increase, investors are shifting their focus to alternatives like the euro, Swedish crown, and Japanese yen.

Risk-on mood pressures safe-haven Yen

Markets have been lifted by China's latest push to boost domestic spending, an initiative aimed at strengthening household incomes and consumption. Adding to the optimism is growing speculation about potential Ukraine peace talks involving US President Donald Trump and Russian President Vladimir Putin. With investors feeling more confident, traditional safe-haven assets like the Japanese Yen are losing some appeal.

At the same time, traders are repositioning ahead of a crucial week for central banks. Both the Bank of Japan (BoJ) and the US Federal Reserve (Fed) are set to announce policy decisions on Wednesday, making this a key moment for currency markets.

Despite its current slide, the Yen may not have much further to fall. Japan's annual Shunto wage negotiations have yielded positive results, fueling expectations that the BoJ will stay on its slow but steady path toward tightening monetary policy. Higher wages are expected to boost consumer spending and inflation, giving the central bank more room to continue shifting away from its ultra-loose stance.

Fed vs. BoJ: Rate divergence in play

One factor that could limit further Yen weakness is the narrowing interest rate gap between Japan and the U.S. Traders are now pricing in multiple Fed rate cuts this year, with reductions expected in June, July, and October. Concerns about a U.S. economic slowdown-driven by potential tariff risks, a cooling labor market, and easing inflation-are fueling expectations that the Fed will start cutting sooner rather than later.

Monday’s U.S. retail sales data reinforced these concerns, with February figures rising just 0.2%-far below the expected 0.7%. This underwhelming consumer spending data strengthens the case for the Fed to pivot toward rate cuts.

Meanwhile, Japan's Finance Minister Katsunobu Kato signalled a more hands-off approach to bond markets on Tuesday, stating that yields should move according to market forces. This follows a record spike in Japan’s 40-year government bond yield, hinting that policymakers may be growing more comfortable with a gradual shift away from extreme monetary easing.

Currency movers: Yen and Euro take the lead

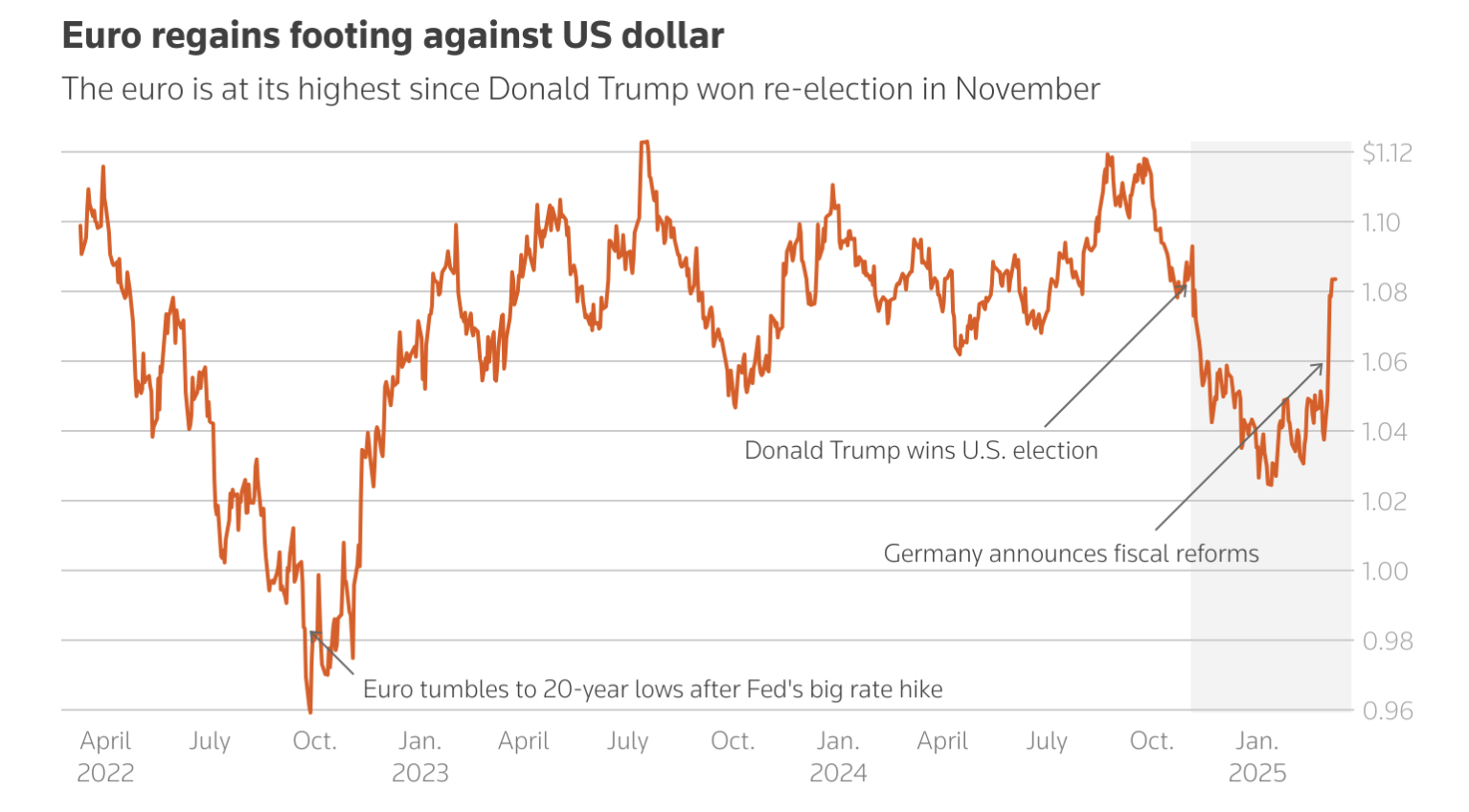

The Euro has also been a standout performer in the global currency market. Germany's historic proposal to ramp up defense and infrastructure spending has propelled the euro to its highest level since the U.S. election, posting its biggest weekly gain versus the dollar since 2009 according to analysts..

With the European Central Bank nearing the end of its easing cycle and European defense spending rising, analysts see further gains ahead, with BofA predicting the euro could reach $1.15 by the end of 2025.

The Japanese yen has been another major gainer, strengthening by approximately 6% against the dollar so far this year. This surge is driven by higher Japanese interest rates and safe-haven demand amid global uncertainty. Investors looking to hedge against a potential U.S. slowdown are turning to Japan due to the likelihood of lower U.S. Treasury yields.

Yen-positive developments at home-including companies meeting union demands for substantial wage increases-could push the BoJ to accelerate rate hikes, further lifting the yen's appeal after four straight years of declines. Speculators have placed their largest-ever bets on the yen continuing to rise.

China’s yuan, despite facing significant tariffs under Trump’s trade policies, has also strengthened this year, trading around 7.25 yuan per dollar. Some expected Beijing to allow its currency to weaken to counteract tariff impacts, as it did during the 2018-2019 trade war. However, China has still managed a relative trade-weighted depreciation against key trading partners, supporting its exporters.

With both the BoJ and the Fed set to take center stage, the USD/JPY pair is in a wait-and-see mode. The direction of the Yen in the coming days will largely depend on the outcome of these central bank decisions-along with any major developments in Ukraine peace negotiations and the evolving impact of Trump’s tariff policies.

Disclaimer:

The information contained within this blog article is for educational purposes only and is not intended as financial or investment advice.

This information is considered accurate and correct at the date of publication. No representation or warranty is given as to the accuracy or completeness of this information.

The performance figures quoted are not a guarantee of future performance or a reliable guide to future performance. Changes in circumstances after the time of publication may impact the accuracy of the information.

Trading is risky. We recommend you do your own research before making any trading decisions.