Gold and silver surge as the debasement trade takes hold

Gold and silver are climbing at a pace that reflects more than a routine haven rally. Their surge has become the clearest expression of the so-called debasement trade - a shift by investors who believe political instability, widening fiscal risks, and weakening currencies are chipping away at real purchasing power.

Silver futures have doubled this year, while gold is up more than 60%, signalling how widespread the flight into hard assets has become.

Copper’s record high above $11,400 per tonne adds weight to this shift, but it is gold and silver that best capture the market’s concern that volatile policy choices can distort the value of money itself. Their rise now hinges on a complex mix of supply constraints, tariff tensions, and expectations of easier monetary policy, setting the stage for a pivotal period ahead.

What’s driving gold and silver higher?

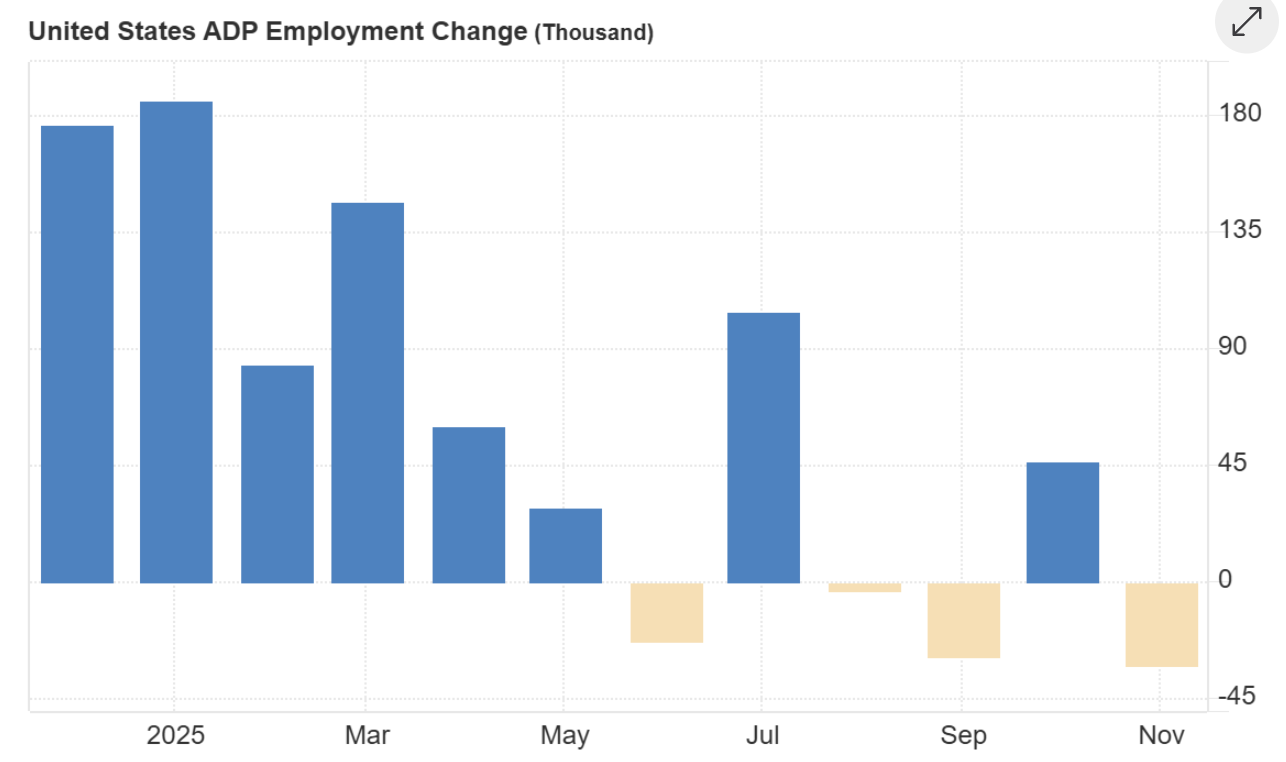

The forces behind the metals rally have intensified in recent months as the economic backdrop weakens. Labour data showing a 32,000 job loss in November - the first negative three-month employment trend since 2020 - has reinforced the sense that the US economy is slowing.

Markets now expect a 25-basis-point rate cut this month, a shift that has pushed the dollar lower and strengthened the appeal of non-yielding assets. Treasury bill yields dipping below the Fed funds rate have added to the impression that policy is turning accommodative again.

Alongside these macro pressures comes a significant structural story, according to analysts. Silver is being driven not by speculative flows but by an extraordinary rise in physical demand, led by India’s imports of around 60 million ounces in October - four times last year’s levels.

Executives describe this as the first period in decades when the physical market is determining price direction. Gold is experiencing its own structural push, with central banks buying 53 tonnes in October alone as countries such as Poland and Brazil diversify away from the US dollar. Supply constraints in both metals are tightening at the same time that demand is accelerating.

Why it matters

The rally in gold and silver is resonating beyond commodity markets because it reflects a broader erosion of confidence in major currencies. Bloomberg reports that the US dollar has fallen nearly 10% since President Trump took office, while the yen and euro have also weakened.

Investors are increasingly worried that erratic policy choices - from tariffs to budget standoffs - could undermine currency stability. Hard assets, such as gold and silver, have become the preferred hedge against this environment, anchoring portfolios where traditional currency hedges appear insufficient.

Some analysts push back on the narrative of broad debasement, arguing that continued global demand for US government debt contradicts claims of a meaningful shift away from the dollar. As one strategist observed, “If the dollar were truly being rejected, Treasury markets would be the first to show it.” Yet that reassurance has done little to stem renewed interest in metals, largely because they offer protection from policy missteps rather than from economic fundamentals alone.

Impact on markets and investors

The surge in silver is reshaping investor behaviour, with bars and coins increasingly treated as long-term holdings rather than trading assets. In the United States, much of the silver accumulated over the past 15 years has barely returned to the market, creating chronic tightness as industrial demand rises. Manufacturers in the solar, electronics, and automotive sectors are securing multi-year supply contracts to shield themselves from escalating costs and the risk of shortages.

Gold’s ascent is influencing both currency and bond markets as investors adjust to the prospect of lower US interest rates. While stronger jobs data last week lent temporary support to the dollar, most traders believe weakening financial conditions and rising geopolitical risks will sustain interest in gold. Trump’s comments on uncertainty surrounding Ukraine peace talks have reinforced a sense that geopolitical stability remains elusive, further boosting safe-haven flows.

Expert outlook

Most analysts expect gold and silver to remain supported into the early part of next year, though both face short-term sensitivity to inflation data and Treasury yields. Friday’s delayed US PCE report will be a critical test: a hotter reading could strengthen the dollar and temporarily cap gold’s advance. Even so, the broader direction of travel for policy points towards easing, which tends to underpin precious metals.

Silver’s outlook is underpinned by a deepening supply deficit, now in its fifth consecutive year and projected to reach up to 95 million ounces in 2025. Mine development leads times of a decade or more, and limited recycling capacity leaves the market exposed to further squeezes. India’s demand will remain a key variable; any sustained buying at current levels could push the market into even tighter territory. Gold, meanwhile, is expected to benefit from ongoing central-bank accumulation and heightened geopolitical uncertainty.

Key takeaway

Gold and silver are rising on a cocktail of currency anxiety, political instability, and tightening physical supply. The debasement trade - once a fringe idea - is now shaping mainstream asset allocation as investors seek protection from unpredictable policy. Supply deficits in silver and renewed gold accumulation by central banks give the rally deeper foundations than many expected. Inflation data and the Fed’s next move will decide how firmly the trend holds into 2026.

Gold and silver technical insights

At the start of writing, Gold (XAU/USD) is trading near $4,223, consolidating just beneath the key $4,240 resistance level. This zone, along with the higher $4,365 barrier, is where traders typically anticipate profit-taking or potential FOMO-driven buying if bullish momentum accelerates. On the downside, support sits at $4,035 and $3,935, and a break below either would likely trigger sell liquidations and a deeper corrective phase.

Price action remains constructive overall, with gold continuing to trade within the upper half of its Bollinger Band range - a sign that buyers still maintain control despite slowing upside momentum. The recent tight clustering of candles suggests the market is pausing rather than reversing, awaiting fresh catalysts to spark the next move.

The RSI, now around 76, is rising gradually above the midline, indicating sustained bullish momentum but edging closer to overbought territory. While this supports the ongoing uptrend, it also hints at limited upside unless gold can decisively clear the $4,240 resistance.

At the start of writing, Silver (XAG/USD) is trading around $58.08, consolidating just below the key $58.69 resistance level. This area often attracts early profit-taking, although a clear break could invite fresh long positioning as momentum traders look to extend the rally. On the downside, support sits at $50.00 and $46.93, and a move beneath either would likely trigger sell liquidations and deepen any corrective swing. Traders using Deriv MT5 may find this range particularly active, as the metal’s elevated volatility continues to create sharper intraday swings.

Price action stays firmly bullish, with silver holding near the upper Bollinger Band following a steep rally. This behaviour underscores persistent buy-side interest even as the market pauses under resistance. With volatility elevated, many traders rely on tools such as the Deriv trading calculator to map margin requirements and calibrate position sizes before entering the next leg of the move.

The RSI is hovering around 78.5, sitting just below overbought territory and highlighting strong yet stretched momentum. That supports the broader uptrend but also hints at possible short-term pullbacks unless silver can break resistance convincingly. A decisive move above $58.69 would likely reset momentum and attract trend followers back into the market.

The performance figures quoted are not a guarantee of future performance.