Gold’s pullback deepens: Will PCE ignite the metal’s next surge?

Gold’s pullback has gathered momentum this week, challenging a market that has rarely paused during its record-setting climb this year. Spot prices slipped to about $4,190 per ounce in Thursday’s Asian session as traders booked profits and shifted into defensive mode ahead of Friday’s delayed PCE release - the inflation gauge the Federal Reserve relies on more than any other.

The tension is clear. Markets now assign a nearly 90% chance of a quarter-point rate cut next week, yet uncertainty surrounding inflation has held back fresh buyers. With real yields easing, the dollar weakening, and central banks quietly amassing gold, the question dominating the market is whether the PCE print will supply the spark required for gold’s next decisive move.

What’s driving gold?

The latest slide reflects a cooling of momentum rather than a shift in the underlying trend. Gold is coming off an extraordinary run, having gained more than 60% year-to-date and broken above $4,000 for the first time only last month.

After such rapid gains, even modest profit-taking can create significant intraday swings, particularly among traders who are reluctant to increase exposure before the Federal Open Market Committee confirms its next policy step.

The ADP employment report, revealing a 32,000 drop in private payrolls - the sharpest fall in more than two and a half years - underscores concerns about a softening labour market and fuels expectations of further easing.

Pressure on the US dollar has added another layer to the story. Rumours that White House adviser Kevin Hassett could replace Jerome Powell pushed the greenback to its weakest level since October, with the Dollar Index sliding to 98.86.

A softer dollar typically supports gold, but the metal’s reaction has been muted as investors await stronger direction from macroeconomic data. Until PCE confirms a sustained cooling of inflation, traders appear unwilling to chase fresh highs.

Why it matters

This pullback is significant because it highlights how closely gold is now tied to monetary policy expectations. Real yields dipped to about 1.83%, down three basis points, offering a natural tailwind for bullion. Yet the reluctance of traders to act shows how sensitive the market has become to even minor shifts in inflation expectations.

ANZ strategist Soni Kumari argued this week that “the market needs a fresh trigger” to extend the rally, and that any slide towards $4,000 would likely attract a new wave of strategic buying.

Gold’s behaviour also reflects deepening investor scepticism about the balance of risks in the US economy. The ISM Services PMI held at 52.6, suggesting pockets of resilience, but slowing orders and weak employment highlight an uneven backdrop.

At the same time, with US fiscal concerns rising and the dollar losing momentum, gold has become a preferred hedge for institutions seeking insulation from policy uncertainty and currency volatility.

Impact on markets and investors

Financial markets are already recalibrating in anticipation of lower rates. Money markets price about an 87% chance of a December cut and nearly 89 basis points of easing by late 2026, implying a Fed Funds Rate of around 2.99%.

This repricing has dragged the 10-year Treasury yield to roughly 4.06%, reinforcing the appeal of non-yielding assets. Lower real rates reduce the opportunity cost of holding gold and strengthen its role as a core portfolio diversifier.

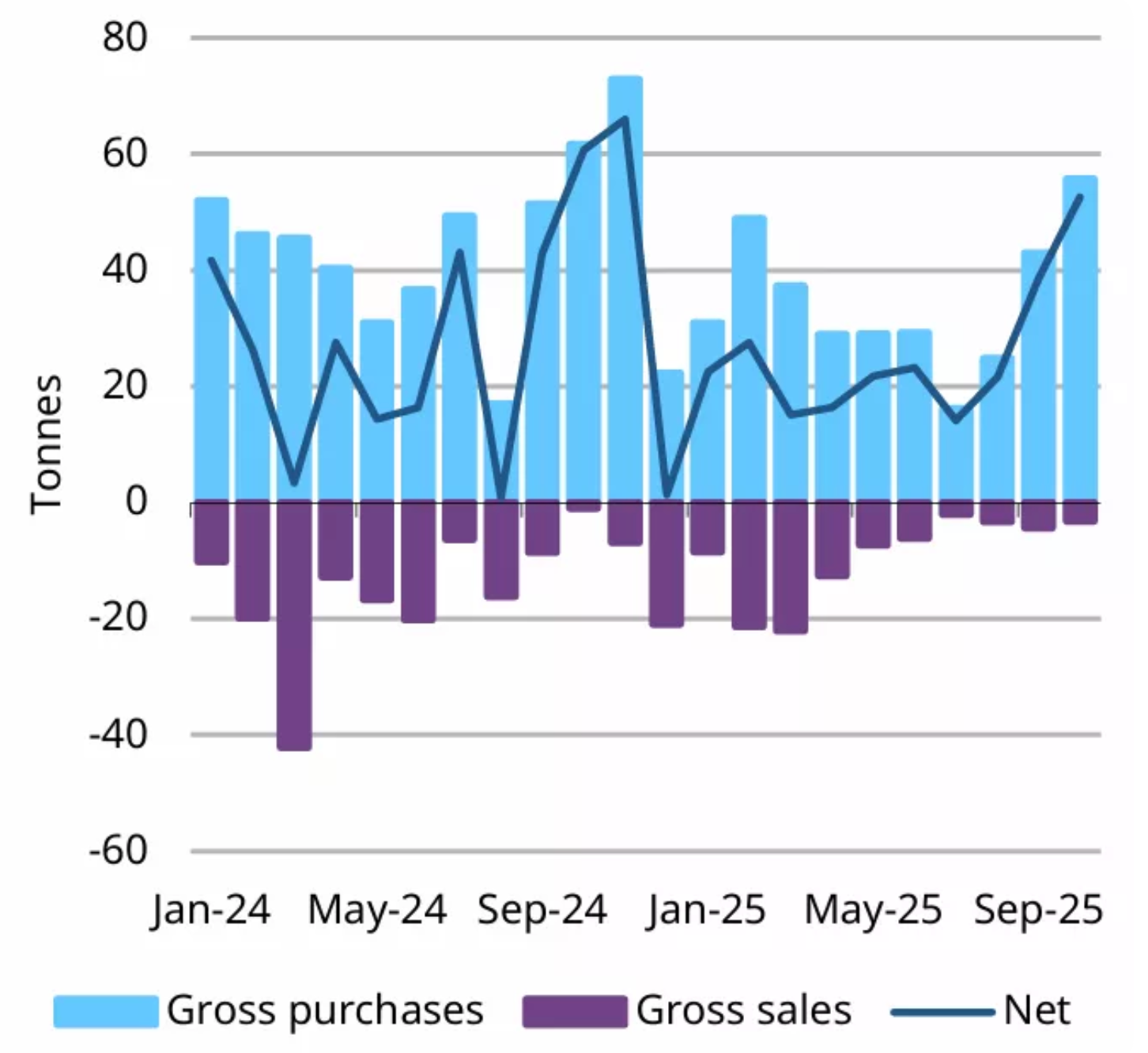

The impact is equally visible in structural flows. Central banks purchased a net 53 tonnes of gold in October - the strongest month of buying so far in 2025, according to the World Gold Council. Poland’s renewed accumulation led the trend, but the message is broader: reserve managers are diversifying away from dollar-denominated assets at a growing pace. For private investors, this creates a floor under prices during moments of market hesitation.

What makes this moment particularly important is the disconnect between short-term caution and long-term optimism. While traders trim their exposure ahead of the PCE, institutional surveys indicate that nearly 70% of global investors expect gold to rise again next year. This combination of tactical indecision and strategic conviction suggests that any data-driven trigger could set off a renewed push higher.

Expert outlook

Analysts remain broadly constructive on gold’s medium-term trajectory. Goldman Sachs expects gold to reach about $4,900 by the end of 2026, arguing that “sticky purchases”, particularly from central banks, are driving a structural revaluation of the asset. Its recent poll of more than 900 clients found that the largest share - 36% - foresee gold above $5,000 by 2026, with only a small minority expecting a retreat below $4,000.

JPMorgan shares this bullish view, projecting prices around $5,055 in the final quarter of 2026, while Morgan Stanley sees the yellow metal at $4,400 by the end of next year. That said, analysts caution that the path will be uneven. Friday’s PCE release, next week’s FOMC meeting, and jobless claims data will shape the immediate narrative. Markets are looking for confirmation that inflation remains on a slower trajectory; if the data cooperate, gold’s next surge may arrive sooner than expected.

Key takeaway

Gold’s pullback reflects caution rather than a change in its fundamental trajectory. Real yields are easing, the dollar is under pressure, and central banks continue to buy aggressively - all factors that support higher prices. The PCE Index now stands as the pivotal data release, capable of shaping expectations for next week’s Fed decision and determining whether gold’s next surge begins. Traders will be watching closely for confirmation that inflation is cooling and the rate-cut cycle is firmly underway.

Gold technical insights

At the start of writing, Gold (XAU/USD) is trading around $4,190, easing slightly after failing to break above the $4,240 resistance level. This zone, along with the higher $4,365 resistance, is where traders typically look for profit-taking or FOMO-driven buying if momentum strengthens. On the downside, the nearest supports sit at $4,035 and $3,935 - with a break below either likely to trigger sell liquidations and deepen the correction.

Price action remains constructive overall, as gold continues to hold above its key support levels despite extended overbought conditions in previous sessions. The slight loss of upside steam suggests the market may be entering a short consolidation phase while waiting for new catalysts such as inflation data or central-bank commentary.

The RSI, previously deep in overbought territory, is now dipping towards the midline near 70, signalling that bullish momentum is cooling but not fully reversing. Meanwhile, the MACD remains positive, though its histogram is gradually flattening - another sign of slowing momentum rather than outright weakness. Overall, gold retains a bullish bias, but upside may be limited unless price can confidently break above $4,240.

The performance figures quoted are not a guarantee of future performance.