Is US jobs data the trigger that markets are waiting for?

Markets are behaving as though they are standing on a fault line, and U.S. jobs data may determine which way the ground shifts. The dollar has slipped towards a two-month low, gold is hovering near record territory after a 64% rally this year, and Bitcoin is increasingly trading like a liquidity asset rather than a speculative outlier.

The delayed U.S. employment reports for October and November arrive at a moment when investors are no longer asking whether growth is slowing, but how quickly policy will respond. With futures markets leaning towards rate cuts in early 2026, the jobs data could be the trigger that forces markets - and the Federal Reserve - to confront that reality.

What’s driving the focus on US jobs data?

The unusual importance of this week’s labour data stems from timing and context rather than the numbers alone. The reports cover a period disrupted by the longest U.S. government shutdown in history, which delayed releases and stripped out several familiar data points.

Even without a complete unemployment breakdown, the figures offer the clearest read yet on how resilient the labour market was as policy uncertainty peaked.

That matters because the Fed’s policy stance now rests heavily on employment, according to analysts. Inflation has cooled unevenly, and officials have signalled that further progress depends on demand softening without triggering a sharp rise in joblessness.

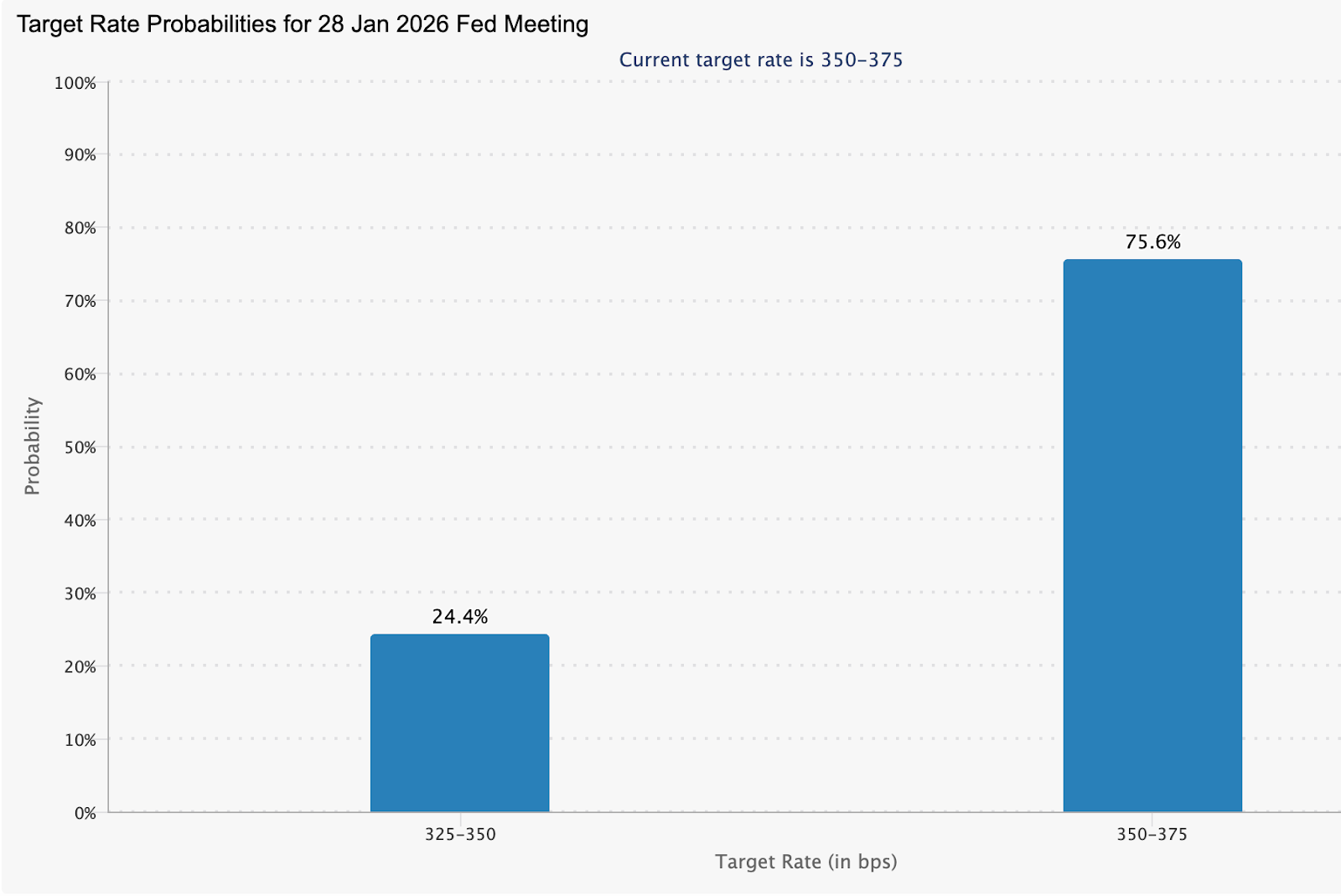

Fed funds futures reflect that tension, with markets pricing a 75.6% probability of a rate hold in January, while quietly building expectations for cuts if labour conditions deteriorate further.

Why it matters

According to analysts, labour data sits at the intersection of growth, inflation and financial stability. Strong hiring gives the Fed cover to keep rates restrictive, while signs of weakness risk exposing how narrow the path has become. Paul Mackel, global head of FX research at HSBC, said the delayed reports would help “give closure on how U.S. employment conditions were panning out during the shutdown,” adding that the dollar remains vulnerable if the data disappoints.

For policymakers, the stakes extend beyond markets. Fed Governor Stephen Miran recently argued that current inflation readings overstate underlying pressure, suggesting price dynamics are closer to the 2% target than headlines imply.

According to experts, job data confirms that labour demand is cooling, weakening the argument for patience, even if inflation has not fully subsided.

Impact on markets, assets and consumers

The dollar has already begun to reflect that uncertainty. The U.S. dollar index slipped to around 98.26 in early Asian trade, while the greenback eased against the yen to 155.07 as traders positioned ahead of the data. Currency markets appear increasingly sensitive to labour signals as rate differentials narrow.

Gold’s response has been more pronounced. After a brief pullback following five consecutive days of gains, spot prices edged higher again to around $4,311 an ounce, supported by a softer dollar and expectations of looser policy, before another minor pullback.

Tim Waterer, chief market analyst at KCM Trade, noted that subdued dollar performance is keeping gold “on the front foot,” with markets questioning whether the Fed is underestimating future rate cuts.

U.S. stock futures, on the other hand, were little changed at the start of the week as investors avoided fresh risk ahead of the delayed November jobs report. Futures linked to the S&P 500 and Nasdaq edged modestly higher after Monday’s losses, while the Dow hovered near flat, signalling caution rather than conviction.

Technology shares led the decline in the previous session as concerns over AI valuations lingered following weak earnings from companies such as Oracle and Broadcom. Those worries, however, have taken a back seat as attention shifts to macro risks. The November nonfarm payrolls report is expected to show a muted gain of around 50,000 jobs, with unemployment seen at 4.4%, numbers that could shape expectations for whether the Fed pauses or accelerates easing in 2026

Crypto markets have taken a different path. Bitcoin and major altcoins slid as traders reduced leverage ahead of the data, triggering more than $470 million in liquidations in 24 hours. Yet history suggests that once labour weakness reshapes policy expectations, liquidity-sensitive assets often recover, sometimes sharply.

Expert outlook

Looking ahead, analysts see asymmetric risks around the jobs data. ANZ has flagged upside risks for gold if employment proves to be a weak spot, suggesting prices could test $5,000 an ounce next year should rate cuts arrive sooner than expected.

The broader challenge is interpretation. This week’s jobs report lands alongside delayed retail sales, CPI, PCE inflation and housing data, all compressed into a narrow window. Markets are likely to react not just to the numbers themselves, but to how consistently they point towards a slowing economy. The jobs data may not deliver clarity on its own, but it could still act as the catalyst that forces expectations to realign.

Key takeaway

U.S. jobs data has become the pressure point where concerns about growth and policy expectations collide. A softer labour picture would reinforce the case for rate cuts, weakening the dollar while supporting gold and liquidity-driven assets. Volatility is likely as multiple delayed releases arrive at once. Investors should watch not just the headline figures, but how decisively they reshape the Fed’s narrative heading into 2026.

Gold technical insights

Gold remains in a constructive but consolidative phase after its sharp rally, with price stalling just below the US$4,365 resistance as profit-taking emerges. Momentum indicators suggest a cooling rather than a reversal: the RSI has eased slightly below 70, signalling that overbought conditions are being worked off, while the MACD remains firmly in positive territory, with a flattening histogram indicating slowing upside momentum rather than outright weakness.

As long as price holds above the US$4,035 support zone, the broader bullish structure remains intact. A decisive break above US$4,365 would likely reignite trend momentum, while a failure to hold key support could expose deeper liquidation towards US$3,935.

The performance figures quoted are not a guarantee of future performance.