黃金價格會因需求上升及2025年首次聯準會降息而飆升嗎?

分析師指出,黃金價格可能持續走高,受到創紀錄的ETF資金流入、關稅推升的通膨壓力,以及聯邦儲備局2025年首次降息的支持。雖然因獲利了結與美元走強短期可能暫停,但需求的結構性驅動因素指向中期價格上漲。

重點摘要

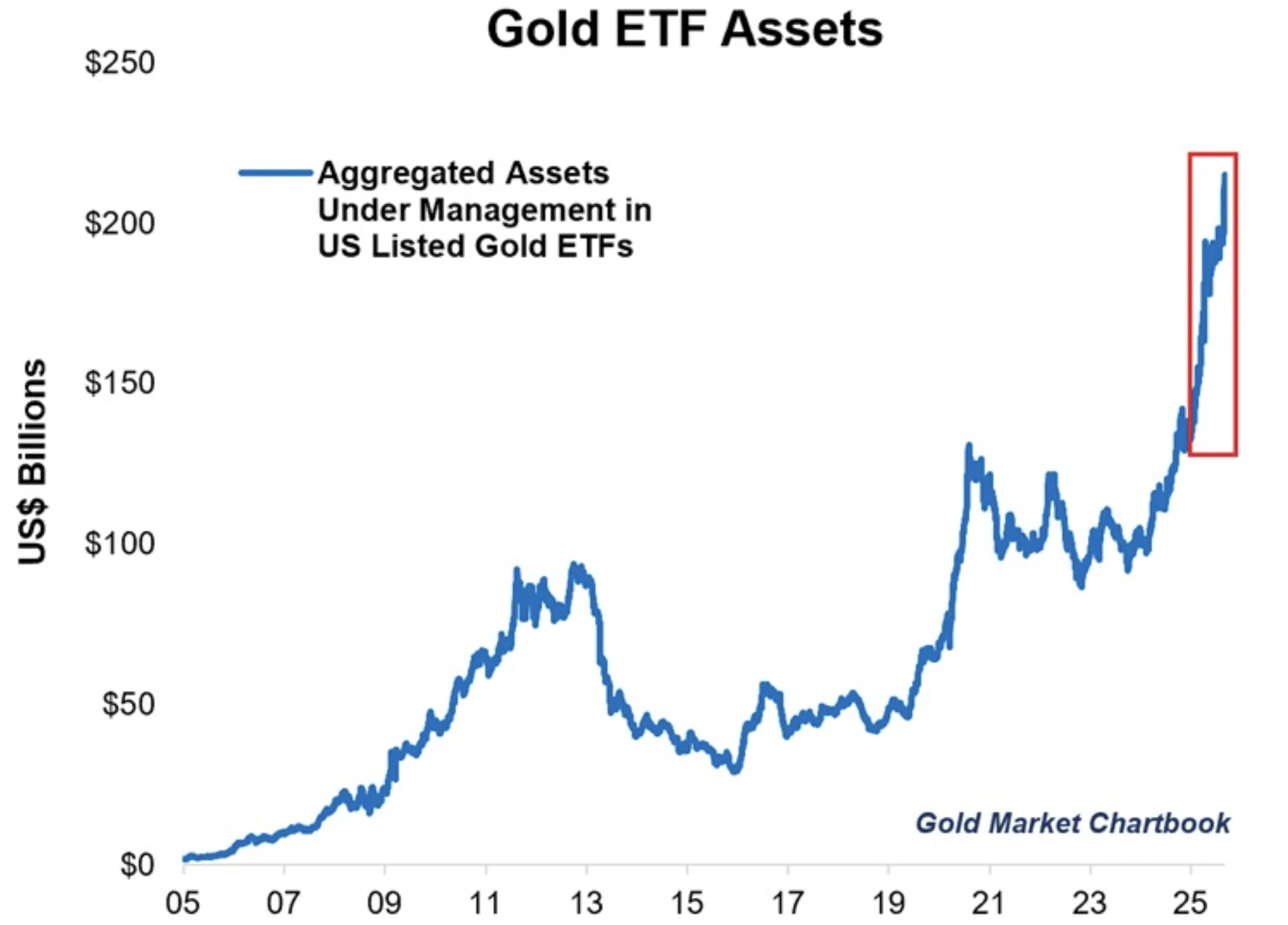

- 美國黃金ETF資產在兩年內翻倍,達到2150億美元,2025年新增279公噸黃金。

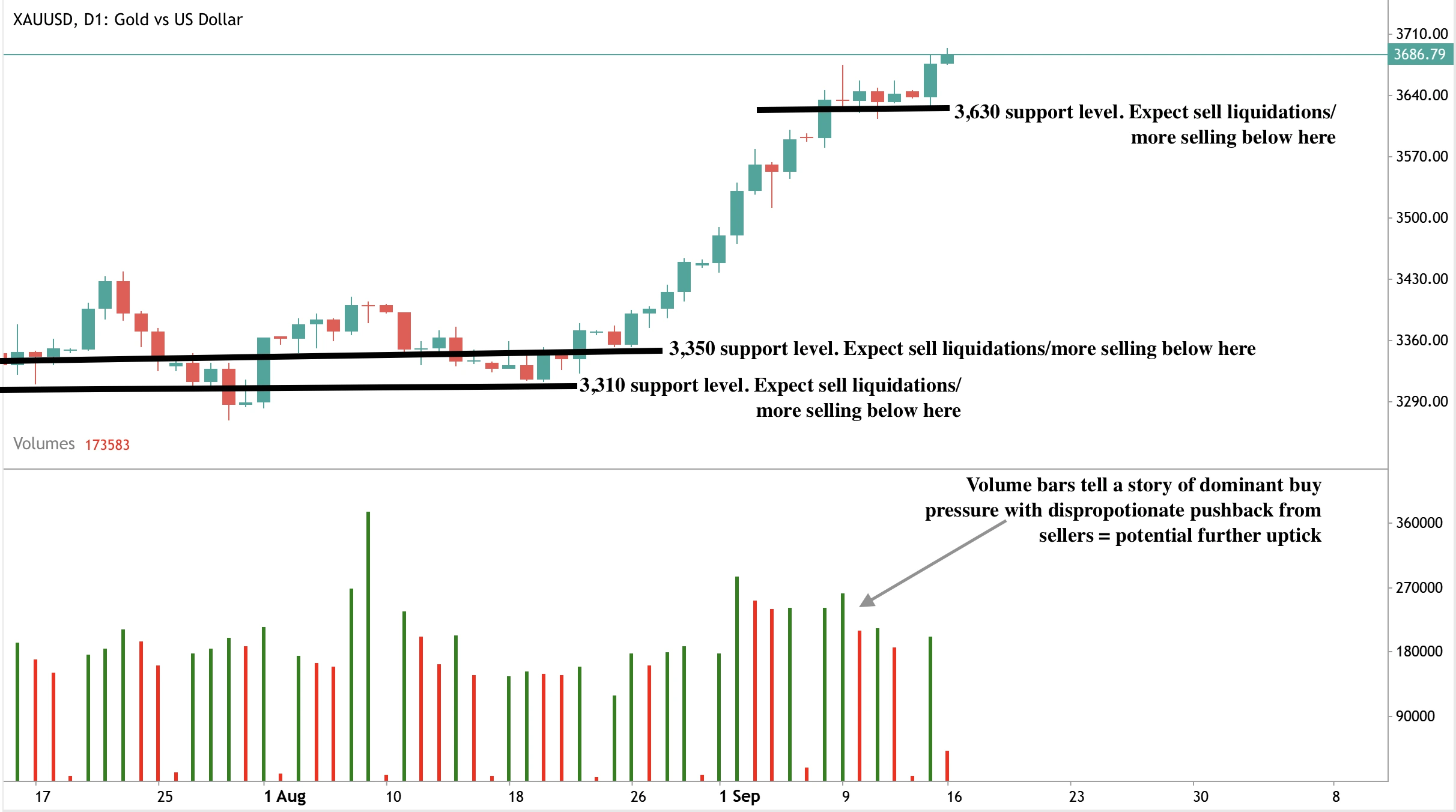

- 現貨黃金交易價格接近3700美元,投資人關注3800美元價位。

- 滲透至消費者價格的關稅預期將推升通膨,歷來為黃金需求的重要驅動力。

- 聯準會預計將進行自一月以來首次降息,降低實質收益率,支持無收益資產。

- 風險包括投機過度持倉、美元走強及聯準會前瞻指引的不確定性。

黃金ETF需求激增

黃金需求激增,美國ETF領先。至2025年9月,美國黃金ETF管理資產達2150億美元,超過歐洲及亞洲ETF合計的1990億美元。今年迄今流入279公噸,凸顯需求規模。

主要基金清楚展現此趨勢。SPDR Gold Shares (GLD) 股價為338.91美元;其52週低點約為2024年9月18日的235.30美元,年內漲幅超過40%。

iShares Gold Trust (IAU) 股價為69.45美元,年增48.11%。這些漲幅反映黃金價格的廣泛反彈,強化ETF需求既反映又放大市場動能的觀點。

關稅作為通膨催化劑

關稅是較少討論但日益重要的驅動因素之一。Sprott Asset Management策略師Paul Wong表示,今年早些時候徵收的關稅仍在供應鏈中發酵。隨著關稅後庫存流向消費者,商品成本預期將上升。

這種通膨衝擊直接呼應黃金作為購買力侵蝕對沖工具的傳統角色。若通膨加速且聯準會降息,實質利率將大幅下降,創下自1970年代以來最有利黃金的環境。Sprott稱之為「貶值交易」——貨幣疲弱與通膨結合,推動資金流入黃金等硬資產。

美國聯邦儲備局9月中旬降息

聯準會預計本週降息25個基點。利率下降降低持有黃金的機會成本,而持續的通膨則增強其吸引力。市場也預期降息將持續至2026年,以避免經濟衰退風險。

但另有政治干預的複雜因素。川普總統多次施壓聯準會要求更大幅度降息,並影響其更廣泛職能。他對聯準會獨立性的攻擊造成制度不確定性,歷史上此類因素會推動投資人轉向避險資產。

黃金回調風險

黃金看漲前景依然穩固,但戰術性回調可能發生。本週美元指數微升0.1%,使以美元計價的黃金對海外買家更昂貴。投機者截至9月9日淨多頭合約減少2445口至166,417口,顯示獲利了結跡象。

KCM Trade分析師Tim Waterer指出,「盤整期或小幅回調可視為健康現象,有助於支持黃金未來挑戰更高價位的目標。」

黃金市場影響與展望

黃金中期走勢仍看好。高盛維持2026年中每盎司4000美元目標,認為風險偏向上行。強勁的ETF需求、關稅推升的通膨及實質收益率下降的可能性均支持此觀點。

全球動態亦支持黃金地位。各國央行持續增加黃金儲備,分散美元風險以強化資產負債表。此累積凸顯黃金作為中立儲備資產的持久角色,尤其在美元主導地位面臨通膨與地緣政治壓力挑戰之際。

黃金價格技術分析

撰文時,黃金價格強勁上漲,日線圖及成交量柱顯示多頭壓力明顯。賣方推力不足。若買方持續推進,可能突破3800美元價位。反之,若出現回落,價格可能測試3630美元支撐,進一步支撐位在3550及3310美元價位。

聯準會前的黃金投資啟示

對投資人而言,布局仍偏多。中期來看,ETF需求、關稅推升的通膨與聯準會降息的匯聚,構成數十年來最強黃金環境之一。央行持續強化需求故事,黃金仍是尋求對抗通膨與政策不確定性投資組合中的關鍵配置。

立即使用Deriv MT5帳戶交易下一波行情。

免責聲明:

所引用的績效數據不保證未來表現。