Silver price forecast: Why the metal's rally has teeth this time

Silver’s rally over the past five days isn’t a false dawn - it’s a move built on fundamentals, not fear, according to analysts. Unlike past speculative spikes, this surge reflects a convergence of monetary easing expectations, tight supply conditions, and surging industrial demand from renewables and semiconductor manufacturing.

With the dollar under pressure and traders pricing in a December rate cut, silver’s recent strength signals the start of a fundamentally driven phase rather than another short-lived burst of optimism.

Key takeaways

- Silver trades near $54.40, extending its strongest rally since October.

- Fed rate cut odds rose to 68%, prompting investors to shift towards non-yielding assets, such as silver.

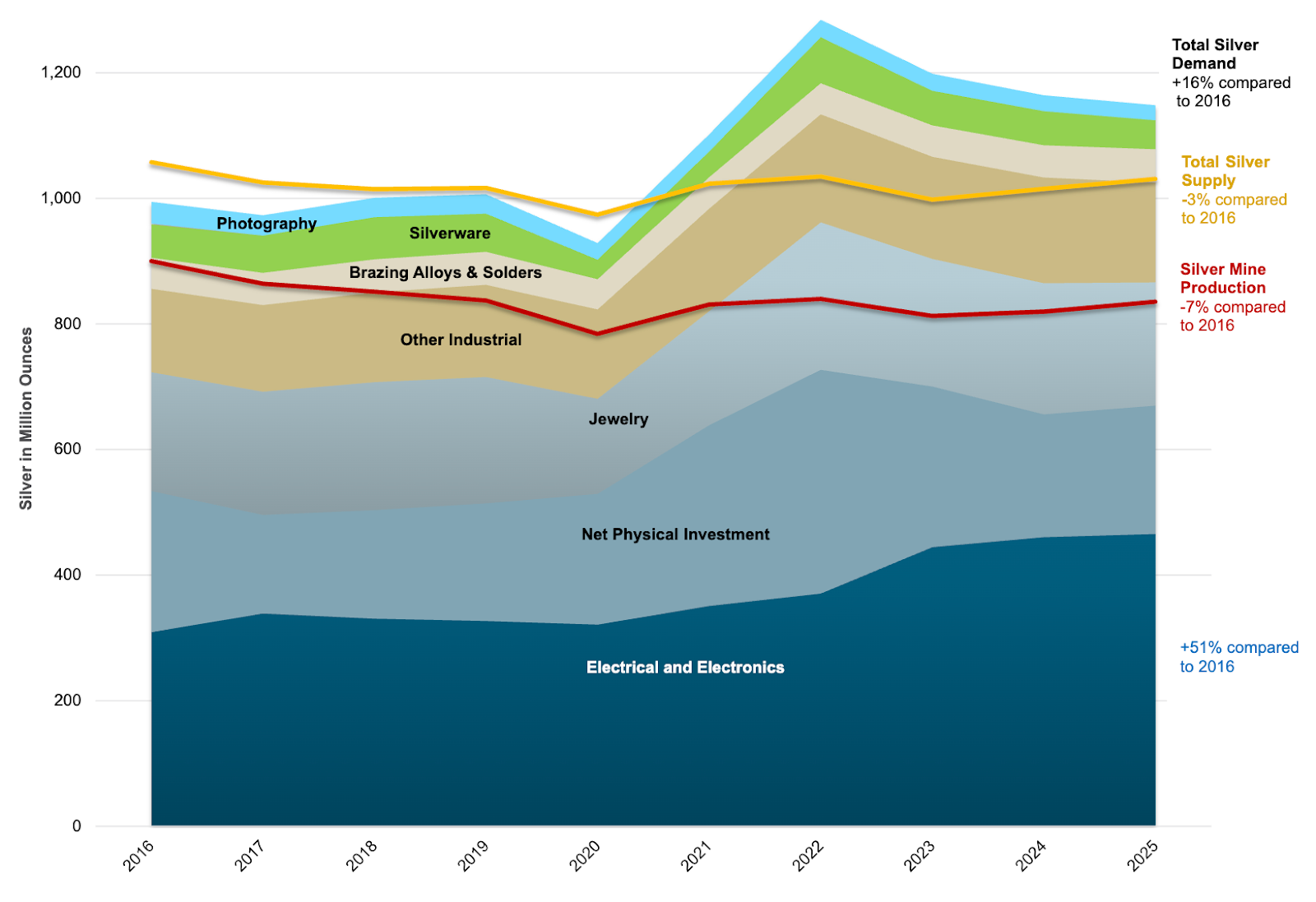

- Mining supply is down 7% since 2016, as industrial demand outpaces production.

- Renewable energy and EV demand now account for over half of total silver consumption.

Silver policy shift and data weakness drives buying

Silver’s latest rally was triggered by a sharp shift in interest rate expectations. Recent U.S. data showed the economy losing momentum - private-sector job creation dropped by around 11,000 per week through late October, according to ADP. The slowdown boosted market confidence that the Federal Reserve will cut rates in December, with odds climbing from 62% to 68%, as tracked by the CME FedWatch Tool.

Lower rates typically weaken the dollar and boost demand for non-yielding safe-haven assets. The U.S. Dollar Index (DXY) has slipped to around 99.60, amplifying gains in gold and silver as investors seek alternatives to low-yielding cash.

Ordinarily, progress on the U.S. government shutdown would have cooled safe-haven demand, but this time, policy expectations outweighed politics. The market is reacting to a broader story: slowing growth and a Fed forced into easing.

Fear to fundamentals: Silver’s supply deficit and demand story

This rally marks a departure from previous episodes driven by speculative trading. According to Sprott Asset Management, silver’s strength is now anchored in structural supply deficits and industrial expansion, not hype. Total mine output has fallen by 7% since 2016, while demand from renewable energy, electric vehicles (EVs), and electronics has risen steadily.

Silver industrial demand continues to outpace supply growth

Over half of silver’s total demand now comes from industrial applications - primarily solar panel manufacturing, semiconductors, and EV components. Supply, however, has not kept pace. Recycling volumes have grown only modestly, and new mining investments remain limited, leaving the market increasingly tight.

As one analyst observed, “This is the first silver rally in years driven more by factories than by fear.”

If you’re planning your trade entry, the Deriv trading calculator helps you estimate margin, swap, and potential profit across Deriv platforms, such as Deriv MT5.

The macro backdrop: Dollar weakness and dovish policy

The broader environment reinforces silver’s strength. The combination of a weaker dollar, falling yields, and soft economic indicators has created an ideal setup for precious metals. The University of Michigan Consumer Sentiment Index dropped to its lowest since 2022, while retail activity has softened, signalling that the Fed’s tightening cycle has reached its limit.

US consumer sentiment

Gold has also contributed to sector momentum, briefly rising above $4,300 per ounce in October. Silver, traditionally more volatile, has benefited from the spillover as investors diversify across metals in anticipation of prolonged monetary easing.

In parallel, copper’s supply squeeze adds weight to the argument that the entire metals complex is entering a supply-led revaluation phase. The same structural shortages seen in copper are now emerging in silver, underscoring a shared narrative: demand growth outpacing production across critical commodities.

Industrial strength: The new driver of the silver cycle

Silver’s dual role - safe-haven and industrial metal - makes it unique among commodities.

While gold depends largely on investor and central bank demand, silver benefits from its role in clean energy and technology supply chains. Solar installations are expected to hit record levels in 2025, while EV adoption continues to accelerate.

Analysts estimate that demand from renewables and electronics will grow faster than mining output for at least the next two years, leading to projected price gains of 34% in 2025 and 8% in 2026. Even modest increases in consumption now trigger outsized price responses due to persistent deficits.

Silver technical insights

At the time of writing, silver (XAG/USD) is testing the $54.30 resistance level, a key zone where profit-taking could increase after a strong bullish rally. The RSI is hovering near 69, approaching the overbought region, which signals potential exhaustion in buying momentum and a likelihood of short-term consolidation or a pullback.

The Bollinger Bands show that price action is hugging the upper band, indicating strong bullish pressure but also a risk of near-term overextension. A decisive break above $54.30 could invite further buying, targeting new highs.

However, failure to clear this level may trigger a retracement toward the $47.00 support level, where buyers could re-emerge. Below that, the next key level sits at $41.28, marking a deeper support zone tied to earlier accumulation.

Risks and potential reversals of silver

Despite the strong outlook, a few risks remain:

- A dollar rebound on stronger U.S. data could temporarily cap gains.

- A slower industrial recovery or reduced rollout of renewables could soften demand growth.

- Short-term profit-taking could trigger volatility around the $50–52 range.

However, these are likely to be temporary corrections rather than trend reversals. Tight supply conditions and solid industrial fundamentals provide a durable floor under the market.

Silver outlook: A rally supported by substance

Silver’s ascent is less about speculation and more about structural change. As monetary policy turns accommodative and industrial demand accelerates, the market is transitioning from a reactive trade to a long-term revaluation.

Analysts expect silver to remain above $50 per ounce in 2025, with a potential retest of October’s $54 peak if rate cuts materialise and industrial activity stabilises. The alignment of macroeconomic easing, green energy expansion, and supply deficits provides this rally with the most credible foundation in over a decade.

Put simply, fear may have sparked it - but fundamentals are now driving it.

The performance figures quoted are not a guarantee of future performance.