Precious metals are on fire but this rally isn’t what it seems

%20(1)%20(1).png)

Precious metals are on fire, but not for the reasons markets usually assume. Data shows that Gold breaking above $4,500 an ounce, silver rising nearly 150% this year, and platinum posting one of the sharpest rallies in decades might resemble a textbook flight to safety. Yet, this surge is not being driven solely by panic, nor by a single macroeconomic trigger.

Instead, the metals complex is reacting to deeper fractures forming beneath the global economy. Monetary policy credibility is weakening, supply chains are tightening in unexpected places, and industrial demand is reshaping how scarcity is priced. Each metal is responding to a different pressure point, and together they are signalling something more structural than a short-lived risk-off move.

What’s driving the precious metals rally?

At the surface level, monetary policy has provided the spark. The US Federal Reserve has cut 75 basis points this year, with markets increasingly convinced that further easing will follow in 2026.

Lower real yields have weakened the US dollar, which recently fell to a near three-month low, making dollar-priced metals more attractive to global buyers.

But rate cuts alone do not explain why silver and platinum are outperforming gold so dramatically. The difference this time lies in physical constraints. Silver has surged through the $70-per-ounce level amid persistent supply deficits and robust industrial demand from the solar energy, electronics, and electric vehicle sectors. Its inclusion on the US critical minerals list has reinforced the idea that silver shortages are structural rather than cyclical.

Platinum’s rally goes further still. The market is experiencing its third consecutive annual deficit, with shortfalls estimated at approximately 692,000 ounces, or nearly 9% of global demand. Above-ground inventories have fallen to about five months of consumption, the lowest since 2020. This is not speculative scarcity - it is measurable, physical tightness.

Why it matters

This rally is significant because it marks a shift in the valuation of precious metals. Analysts note that Gold remains a monetary hedge, reflecting concerns about central-bank independence, inflation credibility, and geopolitical stability. Ongoing tensions involving Venezuela, Russia, and global trade policy have reinforced its role as strategic insurance rather than a tactical trade.

Silver and platinum, however, are increasingly being priced as strategic resources. William Rhind, CEO of GraniteShares, argues that platinum is now viewed “as both a precious metal and a strategic industrial asset”, a distinction that fundamentally alters its valuation framework. When metals are treated as inputs critical to energy transition, manufacturing, and emissions control, price sensitivity changes and volatility increase.

This shift also explains why pullbacks have been shallow. Investors are not merely chasing momentum; they are responding to tightening supply visibility and policy-driven demand that cannot be quickly substituted.

Impact on markets, industry, and investors

Platinum’s resurgence highlights how assumptions about electrification have been challenged. Expectations that electric vehicles would rapidly erode platinum demand have proven premature.

Slower-than-expected EV adoption, combined with stricter emissions standards, has increased platinum loadings in catalytic converters rather than reduced them. Engineers have found that higher platinum content improves durability and performance, especially in heavy-duty and high-temperature environments.

Industrial demand is also broadening. Platinum plays a critical role in hydrogen fuel cells, chemical refining, and industrial decarbonisation. China’s approval of platinum and palladium futures contracts has reshaped global price discovery, with trading volumes on the Guangzhou Futures Exchange now influencing established Western benchmarks.

For investors, this creates an unusual environment. Gold offers stability but limited upside in terms of scarcity, while silver and platinum carry higher volatility tied to industrial cycles and policy decisions. The rally is not uniform, and treating precious metals as a single asset class risks missing the underlying divergence.

Expert outlook

Looking ahead, analysts expect continued support for metals but warn that the drivers are becoming increasingly complex. Zafer Ergezen, a futures and commodities specialist, points to the gold-to-silver ratio falling below 65 as evidence that markets are pricing aggressive rate cuts and stronger industrial demand simultaneously.

Gold’s outlook remains constructive, with Goldman Sachs forecasting a $4,900 base case for 2026, though gains may slow if inflation stabilises. Platinum’s trajectory is more sensitive to supply disruptions in South Africa and shifts in Chinese industrial demand. With production largely price-inelastic, even modest demand surprises could trigger further dislocations. The key risk is no longer oversupply, but rather the limited slack the system has left.

Key takeaway

The precious metals rally of 2025 is not a single story of fear or speculation. Gold reflects monetary unease, silver highlights industrial scarcity, and platinum exposes how fragile concentrated supply has become. Together, they point to a repricing of real-world constraints rather than a temporary risk-off trade. What happens next will depend on rates, inventories, and geopolitics - not sentiment alone.

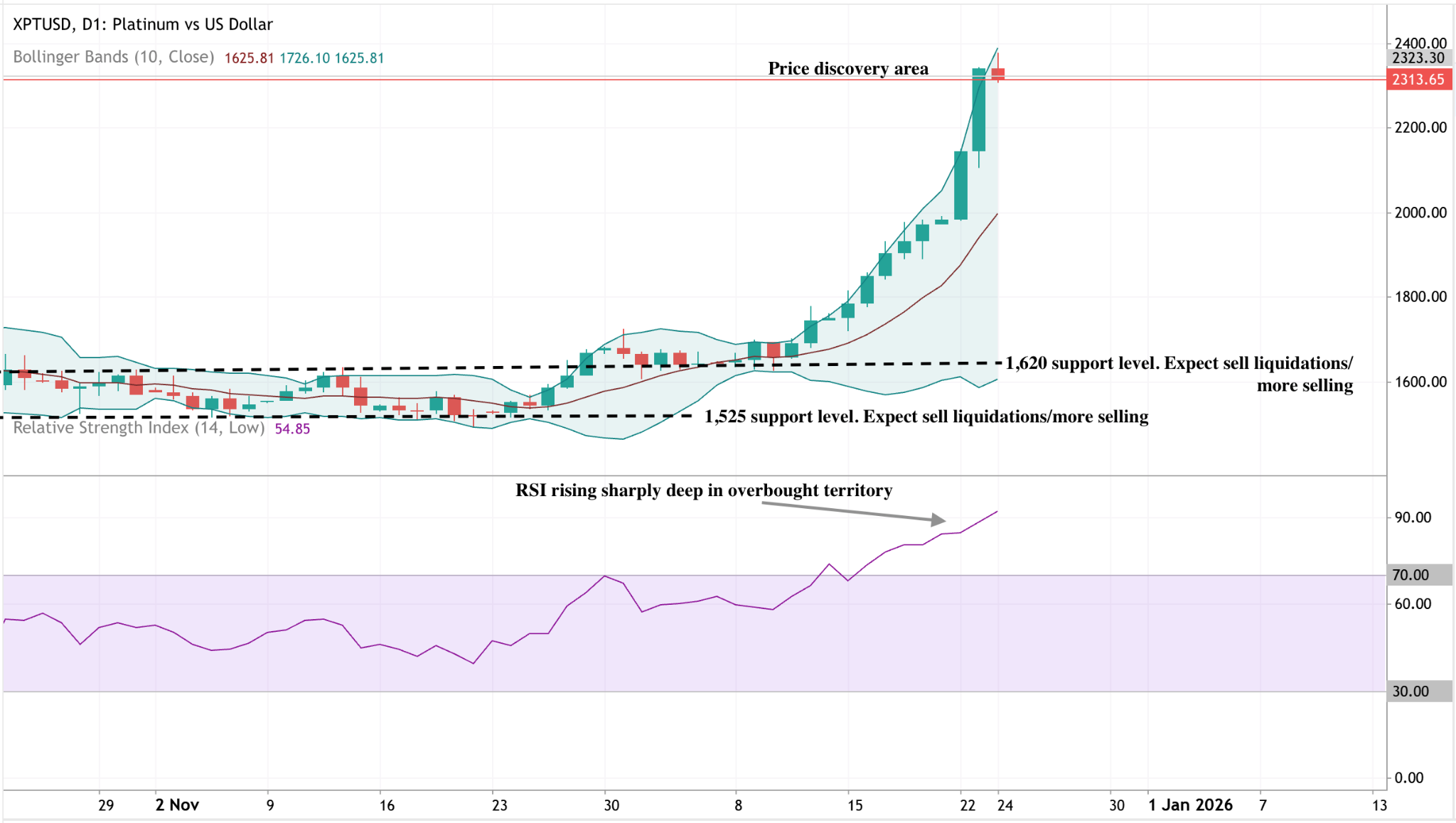

Platinum technical insights

Platinum has surged into price discovery, with price riding the upper Bollinger Band, signalling aggressive upside momentum and strong breakout conditions. The sharp expansion of the bands highlights rising volatility, while pullbacks remain shallow, suggesting buyers are still in control.

On the downside, $1,620 is the first key support, followed by $1,525. A move back inside the Bollinger mid-band would increase the risk of a deeper correction, but for now, momentum remains firmly bullish. The RSI is rising sharply deep into overbought territory, reinforcing strength but also warning of potential short-term consolidation.

The performance figures quoted are not a guarantee of future performance.