Nvidia vs Microsoft: The 2026 outlook for AI market leadership

.png)

Based on current momentum, Nvidia is positioned to take the lead in market valuation by 2026 - potentially becoming the first company closing in on a $5 trillion market cap. Its combination of record earnings, aggressive AI infrastructure investments, and vertical expansion across hardware and software ecosystems gives it a clear edge.

However, Microsoft remains its closest rival, leveraging its AI integration across productivity tools, cloud platforms, and gaming ecosystems to sustain stable, earnings-driven growth. The outcome may hinge on how effectively each company converts AI innovation into long-term revenue resilience.

Key takeaways

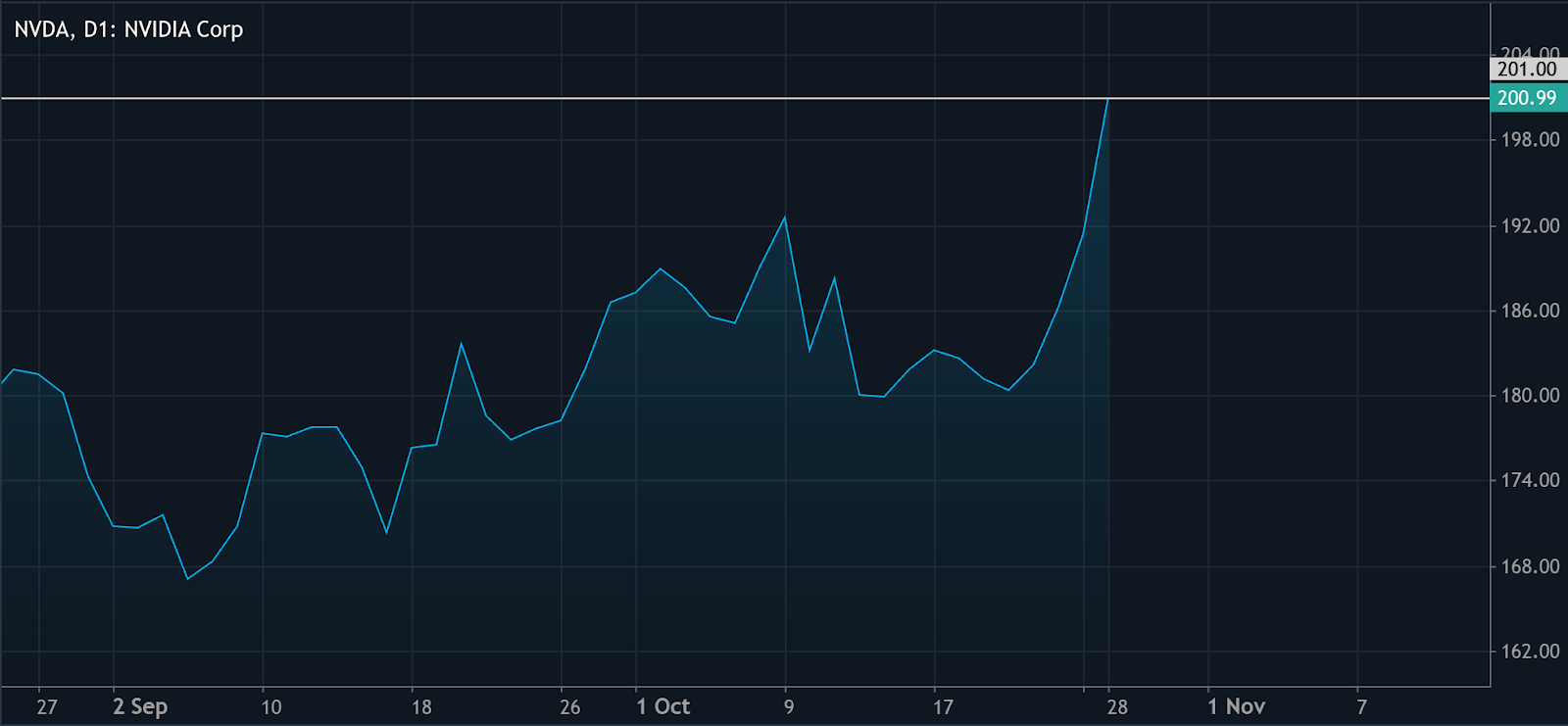

- Nvidia’s market value surged by $230 billion in one day, taking it within 3% of the $5 trillion mark - a first in market history.

- Nvidia’s share price closed at $201.03, up 5% on the day, and is now testing the $210 resistance as investors price in stronger AI infrastructure growth.

- The company announced a $1 billion partnership with Nokia to build AI-powered 5G and 6G networks, expanding its influence beyond data centres.

- Microsoft continues to build AI leadership through Azure, OpenAI partnerships, and the Activision-Blizzard acquisition, reinforcing its diversified model.

- Analysts expect Nvidia to report $4.51 EPS in 2026 and $6.43 in 2027, implying a P/E ratio near 28.7 - relatively modest for its growth rate.

- Both companies could exceed $5 trillion before 2026, but Nvidia’s pure-play AI exposure makes it more sensitive to the next phase of the AI investment cycle.

Nvidia Nokia partnership: Nvidia’s $230 billion day

Nvidia’s stock rally in late October - adding over $230 billion in market value - marks a new phase in the AI investment cycle.

The surge followed the company’s GTC Washington conference, where it announced multiple partnerships and new AI infrastructure projects. The headline deal was with Nokia, where Nvidia committed $1 billion to integrate its AI-RAN (Radio Access Network) systems into next-generation 5G and 6G infrastructure.

This expansion moves Nvidia beyond its traditional GPU dominance into telecom infrastructure, widening its total addressable market. The firm’s strategy mirrors its approach to data centres - owning both the hardware layer and the software stack that powers AI workloads.

Investors can track Nvidia’s price action and volatility directly through CFDs on Deriv MT5.

Race to $5 Trillion market cap: Nvidia’s vs Microsoft’s stability

The competition between Nvidia and Microsoft represents two distinct approaches to AI market leadership:

- Nvidia’s momentum-driven model: Fueled by exponential demand for GPUs, accelerated computing, and partnerships with every major AI player - including OpenAI, Meta, AWS, and Oracle.

- Microsoft’s diversified model: Built on recurring revenues from Azure, Microsoft 365, and gaming ecosystems like Activision-Blizzard, with AI woven throughout its services.

At current valuations, both companies are within reach of the $5 trillion milestone. Nvidia’s faster earnings trajectory - $86.59 billion in trailing 12-month net income - gives it a near-term advantage. Yet Microsoft’s consistent cash flow and balance sheet strength make it more resilient in the event of an AI market slowdown.

AI expansion through strategic partnerships

Nvidia has positioned itself as a central node in the AI economy by investing directly in its ecosystem.

Recent moves include:

- $100 billion investment plan with OpenAI to deploy at least 10 gigawatts of Nvidia systems for next-generation model training.

- $5 billion equity stake in Intel, focusing on joint AI chip and data centre development.

- $1 billion equity investment in Nokia, supporting AI-native 5G/6G networks.

These investments transform Nvidia from a chip supplier into an AI infrastructure conglomerate - similar to how Microsoft evolved from a software company into a diversified tech leader in the 2010s.

Nvidia & Microsoft Earnings and valuation outlook 2026

Nvidia’s forward-looking metrics suggest its valuation may still be grounded in fundamentals:

- Fiscal 2026 earnings estimates: $4.51 per share.

- Fiscal 2027 projections: $6.43 per share.

- Forward P/E ratio around 28–30, assuming price stability near $200.

For Microsoft, consensus expects steady double-digit earnings growth, supported by Azure expansion and monetisation of AI tools across Office, GitHub, and LinkedIn.

If both companies meet current projections, Nvidia could exceed $5 trillion in market cap before mid-2026, while Microsoft may reach that milestone through consistent compound growth over a longer horizon.

Market drivers and risks ahead

The AI market is entering a capital-intensive phase where hyperscalers are increasing infrastructure spending, driving Nvidia’s top-line expansion.

However, potential risks include:

- A slowdown in corporate AI investment if macroeconomic conditions tighten.

- Competitive advances from AMD or custom silicon by hyperscalers.

- Regulatory pressures on AI model deployment that could affect demand.

For Microsoft, the key risk lies in monetisation speed - whether Copilot, Azure AI, and AI-integrated products deliver enough incremental revenue to justify its valuation expansion.

Use Deriv’s trading calculator to estimate price risk exposure to highly volatile AI tech stocks like Nvidia and Microsoft.

Nvidia technical insights

At the time of writing, Nvidia’s stock is trading around the $201 mark, breaking decisively above the upper band of the Bollinger Bands - a sign of strong bullish momentum. However, such a sharp move beyond the upper band often indicates overextension, suggesting the stock could be due for a short-term pullback or consolidation.

The Relative Strength Index (RSI) is rising sharply, currently hovering around 65, and heading towards the overbought region (above 70). This momentum implies that bullish sentiment remains strong, but traders should watch for potential profit-taking once the RSI crosses into overbought territory.

In terms of support levels, Nvidia has established key zones at $180, $174.50, and $168. A break below these levels could trigger sell liquidations and increased downside pressure. Conversely, as long as the stock holds above $180, the current trend remains bullishly intact, though volatility is expected to stay elevated.

Nvidia & Microsoft investment implications

The AI market’s next two years will likely be defined by how fast companies can convert hype into sustained profit growth. Nvidia’s $230 billion single-day gain underscores its dominance in the current cycle, but maintaining that pace requires continuous innovation and client investment.

Microsoft’s diversified model gives it a defensive edge - less volatility, more predictable cash flow - making it a potential co-leader in the long-term AI economy.

For investors, 2026 may mark the first true test of AI’s market maturity: whether hardware-driven earnings (Nvidia) or ecosystem-based monetisation (Microsoft) delivers the stronger foundation for the next decade of growth.

The performance figures quoted are not a guarantee of future performance.